TLDR

- RH stock tumbled 11% after missing Q2 earnings expectations with $2.93 EPS versus $3.18 analyst estimate

- Revenue guidance cut to 9-11% growth from previous 10-13% outlook due to tariff pressures

- Company posted 8.4% revenue growth to $899.2 million but fell short of $906.58 million consensus

- CEO describes housing market as worst in nearly 50 years

- RH shifting production away from China to avoid escalating trade costs

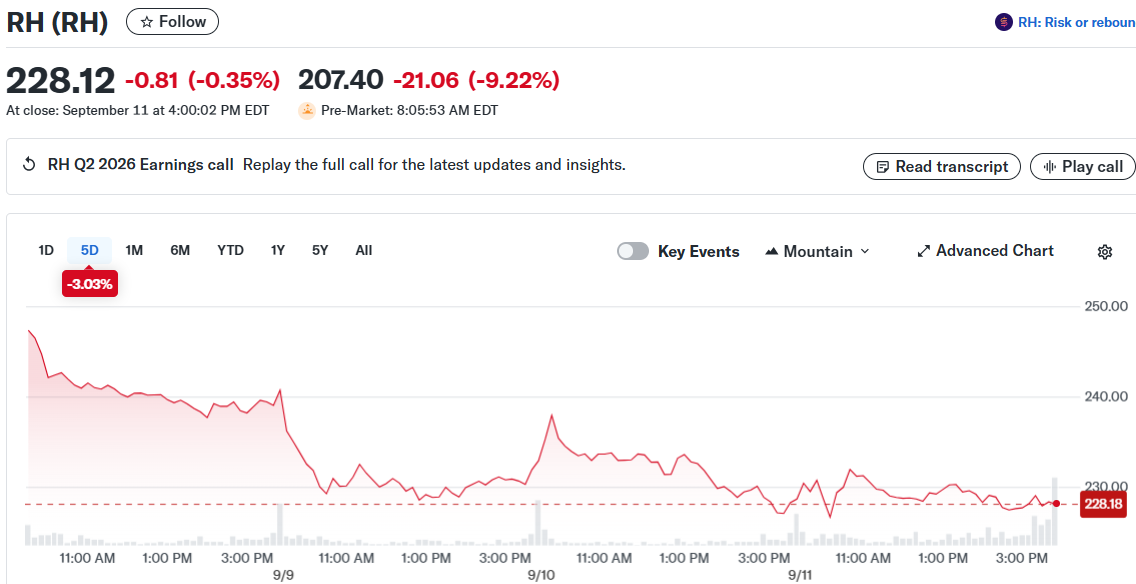

RH shares crashed in premarket trading after the luxury furniture retailer delivered disappointing second quarter results. The stock dropped 11% following an earnings miss and reduced full-year guidance.

The home furnishings company reported adjusted earnings per share of $2.93, missing analyst expectations of $3.18. Revenue reached $899.2 million, representing 8.4% year-over-year growth but falling below the $906.58 million consensus estimate.

Despite the revenue shortfall, RH saw demand increase 13.7% during the quarter. This suggests underlying customer interest remains strong even as external factors pressure results.

Tariff Uncertainty Forces Guidance Reduction

RH lowered its fiscal 2025 revenue growth outlook to 9-11% from the previous 10-13% range. The company cited tariff uncertainties as a primary factor behind the revision.

Third quarter revenue growth is expected between 8-10%. Management set adjusted operating margin guidance at 13.0-14.0% for the full year.

Trade policy changes are reshaping RH’s supply chain operations. The company is rapidly shifting sourcing away from China, with Chinese receipts expected to drop from 16% in Q1 to just 2% in Q4.

Recent 50% tariffs imposed on India are also impacting operations, affecting approximately 7% of RH’s business. These trade cost increases are creating margin pressure across the company’s product lines.

Housing Market Headwinds Impact Luxury Segment

CEO Gary Friedman described current housing market conditions as the worst in almost 50 years. This challenging environment creates headwinds for luxury home furnishing retailers.

When housing market activity slows, demand for high-end furniture typically follows. Consumers become more cautious about major home purchases during uncertain real estate periods.

Despite market challenges, RH achieved some positive financial metrics. Net income surged 79% for the quarter while generating $81 million in free cash flow.

The company maintained adjusted operating margin at 15.1% and adjusted EBITDA margin at 20.6%. Both margins expanded 340 basis points compared to last year, showing operational improvements.

Manufacturing Strategy Shift

RH is accelerating production shifts to its North Carolina factory as part of supply chain reorganization efforts. This move aims to reduce dependence on overseas manufacturing while avoiding tariff costs.

The stock has struggled throughout 2025, falling 42% year-to-date through Thursday’s close before the latest earnings decline. Luxury retailers face particular pressure from both macro-economic factors and trade policy changes.

RH continues navigating between maintaining product quality and managing cost pressures from shifting trade policies. The company’s ability to execute its manufacturing transition while preserving margins will be closely watched by investors.

Get 3 Free Stock Ebooks

Discover top-performing stocks in AI, Crypto, and Technology with expert analysis.

- Top 10 AI Stocks - Leading AI companies

- Top 10 Crypto Stocks - Blockchain leaders

- Top 10 Tech Stocks - Tech giants