TLDR

- JPMorgan upgraded Riot Platforms (NASDAQ:RIOT) from Neutral to Overweight with a price target raised to $19 from $15

- Citigroup also upgraded RIOT to Buy from Neutral, lifting price target to $24 from $13.75

- Both upgrades cite Riot’s pivot into artificial intelligence and high-performance computing as key growth drivers

- JPMorgan assigns 50% probability that Riot secures near-term HPC colocation agreements worth $3.7-8.6 million per MW

- Riot operates 700 MW Rockdale facility and is energizing new 1 GW Corsicana site, positioning it as scaled bitcoin miner

Riot Platforms received a double dose of Wall Street optimism on Friday. Two major investment banks upgraded the bitcoin mining company within hours of each other.

JPMorgan lifted Riot from Neutral to Overweight, pushing its price target to $19 from $15. Citigroup followed suit, upgrading to Buy from Neutral and raising its target to $24 from $13.75.

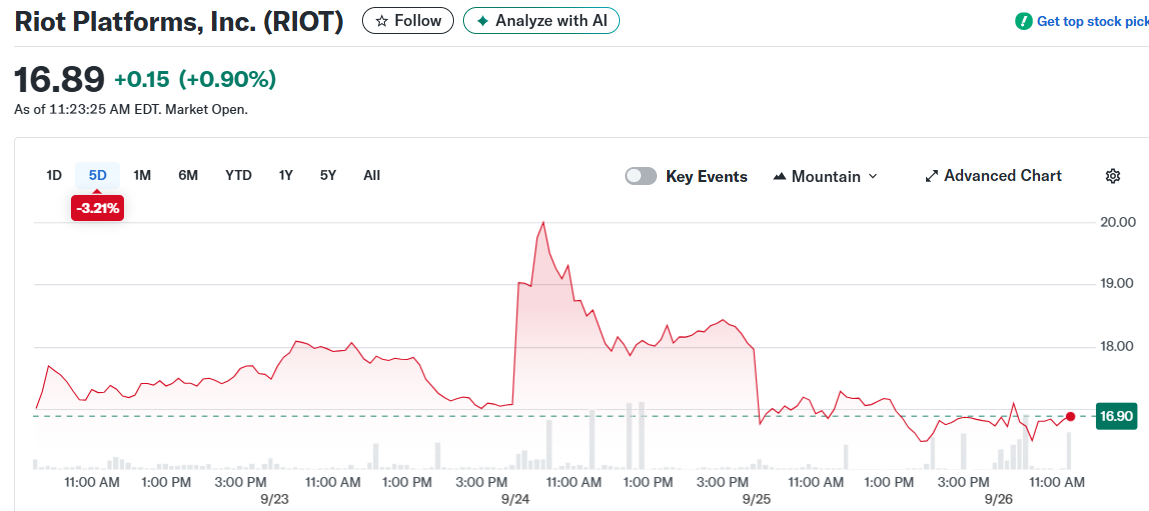

The upgrades come as Riot shares have delivered strong returns over recent months. The stock posted a 112% gain over the past six months despite Friday’s modest decline.

JPMorgan called Riot “the rare bitcoin miner with installed scale, a clear path to hashrate expansion, cheap power contracts, capital and HPC optionality.” The bank highlighted the company’s position as offering “the best value relative to other operators with HPC upside” in its coverage universe.

Both firms pointed to Riot’s strategic shift toward artificial intelligence and cloud services. This pivot comes as traditional bitcoin mining profits face pressure from changing industry economics.

The company operates the 700 MW Rockdale facility, described as one of the largest bitcoin mining facilities in the United States. Riot Platforms is also working to energize its new 1 GW Corsicana site, expanding its operational capacity.

High-Performance Computing Opportunity

JPMorgan analysts assign a 50% probability that Riot will secure near-term high-performance computing colocation agreements. The bank uses Core Scientific’s 800 MW CoreWeave deal as a benchmark for valuation.

HPC colocation contracts carry substantial value, with JPMorgan estimating worth between $3.7 million to $8.6 million per gross megawatt. However, the bank noted that a potential HPC deal “could still be several months away.”

Riot has been positioning itself for these opportunities through recent strategic moves. The company issued convertible debt to purchase bitcoin directly and is actively exploring HPC hosting opportunities.

The mining company reported strong financial results for the second quarter of 2025. Net income reached $219.5 million with adjusted EBITDA of $495.3 million.

Total revenue hit $153.0 million, up from $70.0 million in the same period last year. The increase was driven by an $85.1 million rise in bitcoin mining revenue.

Mining Performance Remains Strong

Riot’s operational metrics continue to show growth. In August, the company produced 477 bitcoin, marking a 48% increase compared to the previous year.

This represented a slight decrease from July’s production of 484 bitcoin. The month-to-month variance is typical in mining operations due to network difficulty adjustments.

The company held 19,309 bitcoin at the end of August. This represents a 93% increase from holdings in the previous year.

Riot’s stock performance stood out in Friday’s trading session. While the broader bitcoin mining sector declined sharply, Riot fell just 1.2% to $16.55.

The contrast was stark compared to sector peers. IREN dropped 9.7% after JPMorgan downgraded it to underweight from neutral.

CleanSpark fell 9.3% following its downgrade to neutral from overweight. The bank maintained its buy rating on Cipher Mining while doubling its price target to $12 from $6.

JPMorgan kept MARA Holdings at overweight but reduced its price objective to $20 from $22. These moves reflect the bank’s selective approach to the mining sector.

Cantor Fitzgerald recently adjusted its Riot price target to $24 from $25 while maintaining an Overweight rating.

Get 3 Free Stock Ebooks

Discover top-performing stocks in AI, Crypto, and Technology with expert analysis.

- Top 10 AI Stocks - Leading AI companies

- Top 10 Crypto Stocks - Blockchain leaders

- Top 10 Tech Stocks - Tech giants