Stock: Dips After Market Sell-Off Despite 200% Year-to-Date Surge")

TLDRs;

- Robinhood stock slides nearly 9% amid a broader tech sell-off triggered by U.S.–China tariff fears.

- Despite the pullback, HOOD remains up over 200% in 2025, outperforming the S&P 500.

- Strong Q2 results and record user growth continue to drive bullish sentiment.

- Analysts remain divided, with some warning that valuation may be overheating.

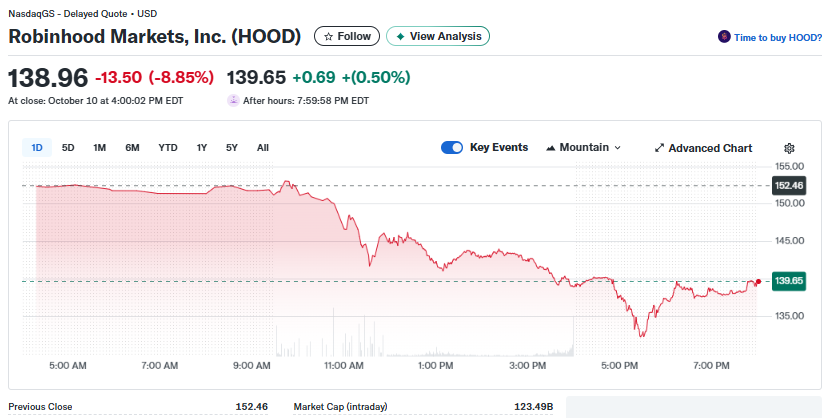

Robinhood Markets (NASDAQ: HOOD) saw its stock dip nearly 9% on October 10, closing at around $139 after a turbulent trading week.

Earlier in the week, shares hit a record high near $153, capping a meteoric run that has seen the stock soar more than 200% year-to-date.

The pullback came as part of a broader market sell-off fueled by renewed U.S. tariff threats against China, which sent tech-heavy indices like the Nasdaq reeling. Despite the sharp drop, Robinhood’s performance in 2025 remains one of Wall Street’s standout stories.

The company’s S&P 500 inclusion in late September catapulted its market capitalization above $100 billion, cementing its place among America’s financial heavyweights.

Earnings Boom and User Surge

Robinhood’s financial results have fueled much of its rally. In Q2 2025, the company reported $989 million in revenue, up 45% year-over-year, and net income of $386 million, more than double the previous year’s figure. Earnings per share came in at $0.42, easily topping analyst forecasts of around $0.30.

Growth in the platform’s core metrics continues to impress. Funded accounts rose to 26.5 million, up 10% from a year earlier, while Robinhood Gold subscriptions surged 76% to 3.5 million members. Average revenue per user climbed 34%, reflecting deeper engagement and diversification beyond trading.

The company’s trailing twelve-month performance underscores its momentum, $3.6 billion in total revenue and $1.8 billion in net profit, representing a remarkable 50% net margin, a rarity in the fintech world.

Analysts Split on Valuation

Despite Robinhood’s strong fundamentals, analysts are increasingly cautious about valuation. The stock trades at a price-to-earnings (P/E) ratio between 62× and 70×, more than double the broader market average.

Consensus estimates peg Robinhood as a “Moderate Buy”, with 12 Buy, 7 Hold, and 1 Sell rating. Wall Street’s price targets vary widely, Barclays at $120, Mizuho at $145, Goldman Sachs at $152, and BofA at $157. While bullish on growth, several firms warn that much of the good news may already be priced in, especially given the recent surge.

Technical signals echo this caution. The stock’s 14-day RSI spiked above 70 (overbought territory) earlier in October before retreating to the 30s, suggesting a near-term cooldown. However, HOOD still trades comfortably above its 50-day and 200-day moving averages ($110 and $79, respectively), confirming a robust uptrend.

Regulation, Rivals, and What’s Next

Beyond earnings, Robinhood faces ongoing regulatory scrutiny and intensifying competition. In January 2025, the firm paid $45 million in SEC fines related to recordkeeping and compliance violations. A subsequent crypto probe was closed without action, a relief for investors wary of stricter oversight.

Meanwhile, rivals are encroaching. Galaxy Digital’s “GalaxyOne” app, launched this month, directly targets Robinhood’s retail investor base with zero-commission stock and crypto trading. Traditional brokerages and newer fintech players like Webull and SoFi are also expanding aggressively.

Yet Robinhood continues to innovate. The company’s recent acquisition of Bitstamp strengthens its global crypto ambitions, while new tokenized stock offerings in Europe and a high-yield “Robinhood Banking” service for Gold members underline its drive to become a one-stop financial “super app.”

Looking ahead, the market will focus on Q3 2025 earnings, set for early November. Analysts expect another quarter of double-digit growth, but warn that short-term traders could lock in profits after the blistering rally.

Get 3 Free Stock Ebooks

Discover top-performing stocks in AI, Crypto, and Technology with expert analysis.

- Top 10 AI Stocks - Leading AI companies

- Top 10 Crypto Stocks - Blockchain leaders

- Top 10 Tech Stocks - Tech giants