Stock: Earnings Report Today Expected to Show 88% Revenue Growth")

TLDR

- Robinhood reports Q3 2025 earnings today with analysts expecting EPS of $0.54 versus $0.17 a year ago and revenues of $1.21 billion, up 88% year-over-year.

- HOOD stock has surged 267% year-to-date, driven by growth in user accounts and increased cryptocurrency trading activity.

- Transaction-based revenues, which make up over 60% of total revenues, are expected to reach $756.4 million, up 137% from last year.

- Options traders anticipate a 9.45% stock price swing in either direction following the earnings announcement.

- Analysts maintain a Moderate Buy rating with KeyBanc raising its price target to $155 and TipRanks AI setting a target of $166.

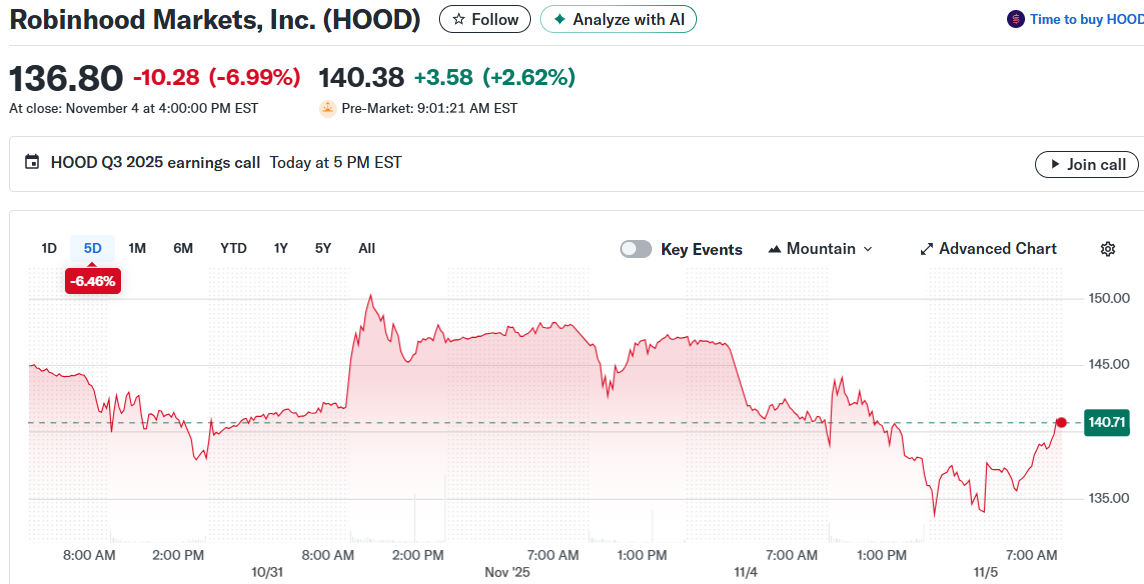

Robinhood Markets reports its third quarter 2025 earnings today after market close. The trading platform has been on a tear this year.

Wall Street analysts expect the company to post earnings per share of $0.54. That’s compared to $0.17 in the same quarter last year. Revenue projections sit at $1.21 billion, representing an 88% jump from the prior year period.

The stock has climbed 267% year-to-date. That puts it well ahead of competitors like Charles Schwab and Interactive Brokers. The rally has been fueled by increased trading activity and a surge in cryptocurrency transactions.

Transaction-based revenues form the backbone of Robinhood’s business model. These revenues account for more than 60% of total net revenues. Analysts expect this segment to reach $756.4 million in Q3, up 137% from last year.

The third quarter saw robust trading volumes across the board. The S&P 500 Index advanced nearly 8% during the period. Major indices repeatedly hit record highs as investor confidence grew.

The Federal Reserve’s rate cut in mid-September didn’t dampen the party. Trading momentum remained strong across equities, fixed income, and digital assets. Cryptocurrencies saw particularly strong interest from both retail and institutional investors.

Breaking Down the Revenue Mix

Options trading revenue is projected at $300.2 million, up 48.6% year-over-year. Equity transaction revenues should hit $82.5 million, representing a 122.9% increase. The real star might be crypto, though.

Cryptocurrency transaction revenues are estimated at $313.9 million. That would mark a 414.6% jump from the same quarter last year. The crypto market has benefited from favorable regulatory developments and growing mainstream adoption.

KeyBanc analyst Alex Markgraff raised his price target on the stock to $155 from $135. He maintained his Buy rating and cited stronger product updates and better monetization trends. His outlook for fiscal year 2026 appears positive.

What Options Traders See

Options traders are pricing in a 9.45% move in either direction following the earnings report. That suggests the market expects a meaningful reaction to the results. Given the stock’s recent volatility, that’s not surprising.

The consensus rating from Wall Street analysts stands at Moderate Buy. Out of 18 analysts covering the stock, 13 have Buy ratings, four have Hold ratings, and one has a Sell rating. The average price target of $144.29 implies a slight downside from current levels.

Robinhood has a solid track record when it comes to earnings surprises. The company has only missed estimates once in the past nine quarters. That consistency has helped build investor confidence.

Interest income likely provided an additional boost during Q3. Interest rates remained relatively high despite the September rate cut. This benefited Robinhood’s net interest revenue line.

The company has been investing heavily in platform upgrades and AI-driven tools. These expenses have kept operating costs elevated. Investments in customer support and regulatory compliance continue as well.

Interactive Brokers and Charles Schwab already reported their Q3 results on October 16. Interactive Brokers posted adjusted EPS of 57 cents, beating estimates. Charles Schwab delivered $1.31 per share, crushing expectations with a 70% year-over-year increase.

Both competitors benefited from increased trading volumes and higher net interest revenues. Their results suggest favorable conditions for brokerage firms during the quarter. Robinhood operates in the same environment.

The Zacks Consensus Estimate for earnings has remained unchanged over the past seven days at 51 cents per share. Revenue expectations have also held steady at $1.21 billion.

Get 3 Free Stock Ebooks

Discover top-performing stocks in AI, Crypto, and Technology with expert analysis.

- Top 10 AI Stocks - Leading AI companies

- Top 10 Crypto Stocks - Blockchain leaders

- Top 10 Tech Stocks - Tech giants