Stock: Fed Rate Cuts Drive Shares To All-Time Highs. Here’s Why")

TLDR

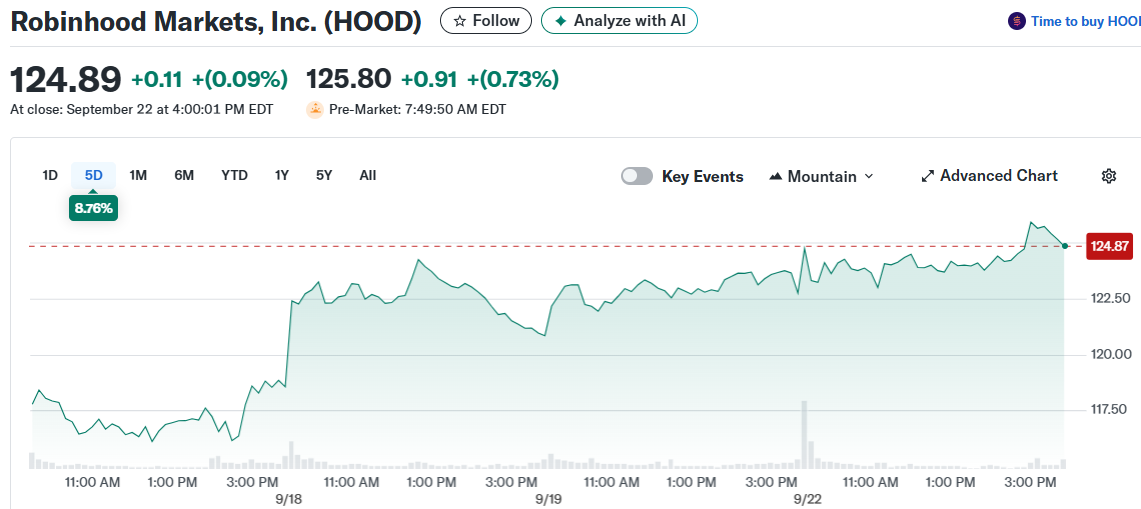

- HOOD stock hits all-time high of $124.89 after Federal Reserve cuts interest rates

- Revenue growth accelerated 45% year-over-year to $989 million in latest quarter

- Net deposits exploded 99% higher while user base expanded to 26.5 million accounts

- Average revenue per user climbed 34% to $151 as customer quality improves

- Stock trades at 61.4x P/E ratio with analyst price targets ranging from $47 to $145

Robinhood stock surged to record levels following the Federal Reserve’s interest rate cut decision. The trading platform closed at $124.89, representing new all-time highs as investors anticipate increased retail trading activity.

The rate cut environment creates perfect conditions for Robinhood’s business model. Lower borrowing costs reduce pressure on retail traders while sparking market volatility that drives trading volumes.

Financial sector stocks led the S&P 500 higher after the Fed announcement. Robinhood positioned itself at the center of this rally as the primary platform for retail investors entering the market.

Recent earnings results validate the stock’s momentum with impressive growth across key metrics. Net revenues jumped 45% year-over-year to $989 million, a remarkable achievement for a company now valued at $107.4 billion.

Strong Financial Performance Drives Growth

Net assets under management reached $279 billion, powered by net deposits that grew 99% year-over-year. This data indicates new users are bringing substantially more capital than previous customer cohorts.

The platform’s funded accounts expanded 10% year-over-year to 26.5 million users. However, the quality of these customers represents the more compelling story behind the numbers.

Robinhood has evolved beyond its beginner platform reputation. The growing net asset base suggests more affluent investors now consider the platform suitable for serious investment strategies.

Average revenue per user hit $151, marking a 34% year-over-year increase. This metric directly impacts profitability and demonstrates the company’s ability to monetize its growing user base more effectively.

Rising market activity should push this figure even higher. The combination creates a positive cycle where increased trading drives both volume and per-user revenue growth.

Valuation Concerns and Analyst Views

HOOD stock currently trades at a 61.4x price-to-earnings ratio compared to the 17.6x financial sector average. This premium valuation raises questions among traditional value-focused investors.

Growth investors defend the multiple based on the company’s performance trajectory. They argue that premium valuations often reflect premium business execution and future earning potential.

Analyst opinions remain divided on the stock’s prospects. The consensus price target stands at $101.88, suggesting potential downside from current levels.

Mizuho analyst Dan Dolev shows more optimism with his September 2025 research note. He maintained an Overweight rating alongside a $145 price target, implying 20% upside potential.

The Federal Reserve’s policy shift provides the macro backdrop for continued business expansion. Historical patterns show retail trading activity typically increases during rate-cutting cycles.

Account openings have already accelerated following the rate announcement. Fresh capital inflows mirror patterns seen in previous accommodative monetary policy periods.

The company’s 52-week trading range spans $22.05 to $126.64, highlighting the dramatic price appreciation over the past year. Current levels sit near the upper end of this range.

Multiple business tailwinds support Robinhood’s growth outlook. Lower interest rates, increased market volatility, and returning retail investor enthusiasm all contribute to revenue expansion potential.

Net deposits grew 99% year-over-year, exceeding analyst expectations for the quarter and demonstrating strong customer engagement with the platform.

Get 3 Free Stock Ebooks

Discover top-performing stocks in AI, Crypto, and Technology with expert analysis.

- Top 10 AI Stocks - Leading AI companies

- Top 10 Crypto Stocks - Blockchain leaders

- Top 10 Tech Stocks - Tech giants