Stock: Shares Plunge 12% as SpaceX Gets Launch Approval Boost")

TLDR

- RKLB stock dropped 12% Wednesday following FAA approval for expanded SpaceX Falcon 9 launches

- Company posted record Q2 revenue of $144.5 million, up 36% year-over-year

- Stock remains up 70% year-to-date with strong institutional support from 540 mutual funds

- Analysts maintain Strong Buy rating with price targets ranging up to $60

- Neutron rocket development on track for late 2025 launch despite competitive pressure

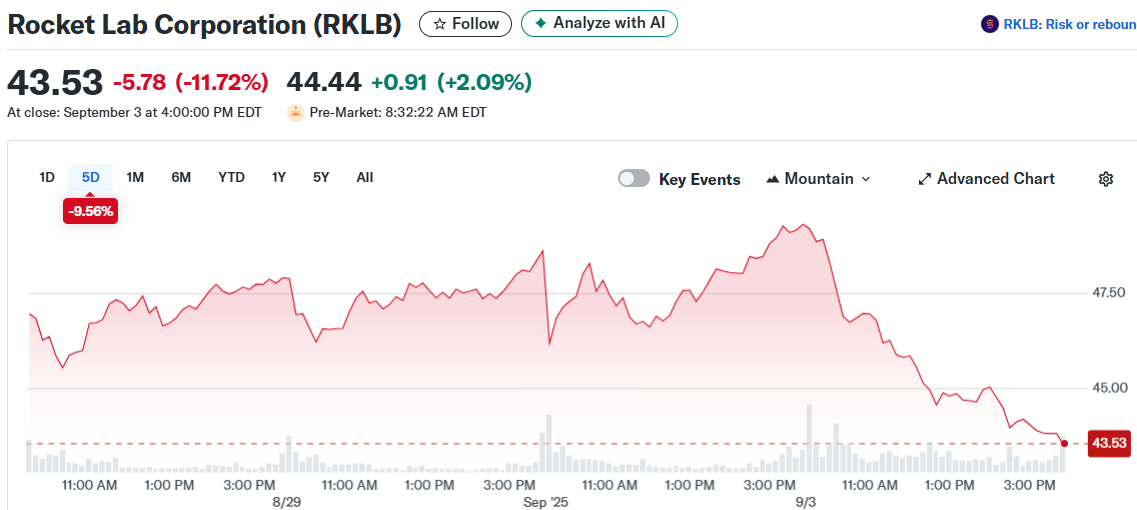

Rocket Lab stock crashed 12% Wednesday as investors reacted to news that SpaceX received regulatory approval to double its Falcon 9 launch frequency. The decline came despite no negative company-specific developments.

The FAA’s decision to expand SpaceX operations from Florida creates additional competitive pressure for Rocket Lab. The Falcon 9 will directly compete with Rocket Lab’s upcoming Neutron rocket when it launches in late 2025.

Rocket Lab stock recovered 2.7% in Thursday pre-market trading. The rebound suggests investors view Wednesday’s selloff as an overreaction to routine regulatory news.

Strong Financial Performance Continues

The space company delivered record second-quarter revenue of $144.5 million, representing 36% growth year-over-year. Revenue came from both launch services and satellite manufacturing divisions.

Rocket Lab has completed 70 launches and deployed 233 satellites across its three operational launchpads. The company’s most recent mission launched from New Zealand in late August.

Losses widened to 13 cents per share in Q2, the largest deficit in eight quarters. However, analysts expect rapid improvement with projected losses of eight cents in Q3.

Management guided for third-quarter revenue between $145 million and $155 million. CEO Peter Beck expressed confidence that strategic investments will drive future profitability.

Wall Street forecasts full-year 2025 losses of 43 cents per share, improving to nine cents in 2026. The projections indicate Rocket Lab is approaching break-even operations.

Analyst Support Remains Strong

Roth MKM analyst Sujeeva De Silva raised his price target from $50 to $60 with a Buy rating. He highlighted progress on Neutron development and completion of launchpad infrastructure.

The analyst consensus shows nine Buy ratings and three Holds over the past three months. Average price targets sit at $30.20, though individual estimates reach much higher.

Rocket Lab holds a 99 IBD Relative Strength Rating, the maximum possible score. The stock has gained 81% year-to-date, outperforming most aerospace peers.

Institutional buying remains heavy with an A+ Accumulation/Distribution Rating. Mutual fund ownership increased for four straight quarters, reaching 540 funds by June.

Technical Picture Shows Consolidation

The stock is forming an early-stage consolidation pattern with a potential buy point at $53.44. Wednesday’s decline brought shares near the 21-day moving average while holding above the 50-day line.

Trading volume spikes on up days as institutions accumulate positions. The 1.5 up/down volume ratio over 50 days indicates positive demand trends.

Management owns 11% of outstanding shares, demonstrating leadership confidence. The insider ownership aligns executive interests with shareholder returns.

Rocket Lab’s 21-day Average True Range of 7.4% reflects the stock’s volatile nature. Daily swings remain common as the company transitions from development to commercial operations.

The company continues advancing its Neutron rocket program for late 2025 deployment. Both Electron and Neutron vehicles feature reusable components to reduce launch costs and improve margins.

Get 3 Free Stock Ebooks

Discover top-performing stocks in AI, Crypto, and Technology with expert analysis.

- Top 10 AI Stocks - Leading AI companies

- Top 10 Crypto Stocks - Blockchain leaders

- Top 10 Tech Stocks - Tech giants