Stock Rallies Hard But Analysts See Cracks in the Foundation. Here’s Why")

TLDR

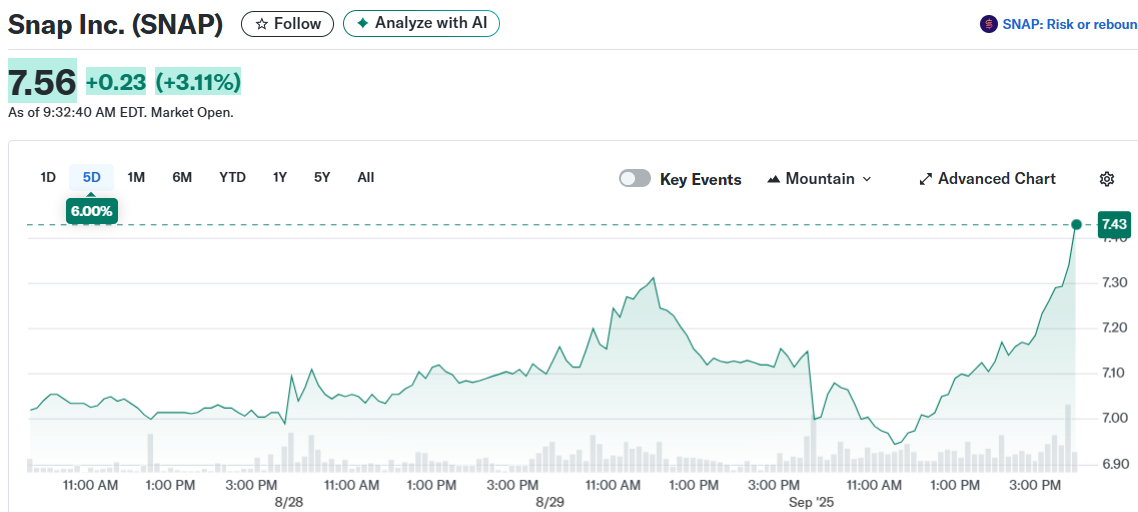

- Snap stock climbed 2.7% to $7.33 on heavy volume after hitting 52-week low of $6.90

- Guggenheim maintains Neutral rating citing slowing global user growth of 2.3% in Q3 vs 3.9% in Q2

- North American audience showing 1.5% annual decline with downloads falling 29.8% in the quarter

- Company issued $550 million in senior notes while analysts expect Q3 daily active users to reach 476 million

- Recent earnings disappointment and ad platform issues continue to weigh on investor sentiment

Snap stock staged a modest comeback Tuesday, climbing 2.7% to close at $7.33 after touching a 52-week low earlier in the session. The recovery came on unusually heavy trading volume of 102.7 million shares, more than double the three-month average.

The bounce occurred even as broader tech stocks retreated. The Nasdaq fell 0.8% while other social media names showed mixed results.

But beneath the surface rally, fresh data suggests deeper problems. Guggenheim maintained its Neutral rating on the stock, pointing to concerning user growth trends that could spell trouble ahead.

Slowing User Growth Raises Red Flags

The investment firm’s analysis of Snap’s advertising platform data reveals a troubling slowdown in user acquisition. Global audience growth dropped to just 2.3% in the third quarter so far, down from 3.9% growth in the second quarter.

Download trends paint an even bleaker picture. Global app downloads declined 12.6% in Q3, worse than the 5.5% drop seen in the previous quarter.

North America remains particularly weak. The domestic audience showed a 1.5% annual decline in Q3, deteriorating from the 1.1% drop in Q2. Download numbers in the region plunged 29.8% compared to 28.5% in the prior quarter.

Guggenheim expects Snap to report 476 million daily active users for Q3. That would represent 7 million net additions and 7.4% growth, marking a deceleration from the 8.6% growth posted in Q2.

Geographic Split Shows Uneven Performance

The user growth story varies dramatically by region. Rest of World markets are projected to add 6 million users in Q3, providing most of the company’s growth momentum.

Meanwhile, North American metrics continue their sequential decline for the third straight quarter. This geographic split matters because North American users typically generate higher advertising revenue per user.

The company recently completed a $550 million debt offering through 6.875% senior notes due 2034. Snap expects to net approximately $541.3 million after expenses from the private placement.

Analyst sentiment remains mixed following the disappointing Q2 earnings report. The results showed slower revenue growth and technical problems with the advertising platform that hurt performance.

Freedom Broker upgraded the stock from Hold to Buy despite the earnings miss, though it cut the price target to $9.00. RBC Capital also reduced its target to $10.00 from $12.00 while maintaining a Sector Perform rating.

A pending class-action lawsuit alleging the company misled investors about advertising performance adds another layer of uncertainty. The legal challenge focuses on claims about ad delivery capabilities that may not have matched reality.

Trading volume patterns suggest investors remain divided on the stock’s prospects. Some view the recent selloff as creating a potential buying opportunity near 52-week lows.

The heavy volume accompanying Tuesday’s bounce indicates heightened interest, though whether this represents bargain hunting or distribution remains unclear. The stock has shown volatility throughout the year as investors grapple with the company’s path back to sustainable growth.

Snap’s advertising platform continues to face technical challenges that have impacted campaign performance. These issues contributed to the disappointing Q2 results and remain a key focus for management heading into the next earnings cycle.

Get 3 Free Stock Ebooks

Discover top-performing stocks in AI, Crypto, and Technology with expert analysis.

- Top 10 AI Stocks - Leading AI companies

- Top 10 Crypto Stocks - Blockchain leaders

- Top 10 Tech Stocks - Tech giants