Stock: Surges 14% After Crushing Q2 Earnings Beat")

TLDR

- Snowflake beats Q2 estimates with 35¢ EPS vs 27¢ expected on $1.14B revenue

- Stock jumps 14% premarket, adding $11B+ to market cap

- Raises 2025 product revenue guidance to $4.4B from $4.33B

- AI demand drives strong Azure cloud momentum in Europe and Africa

- Analysts boost price targets to $280 (Evercore) and $276 (BTIG)

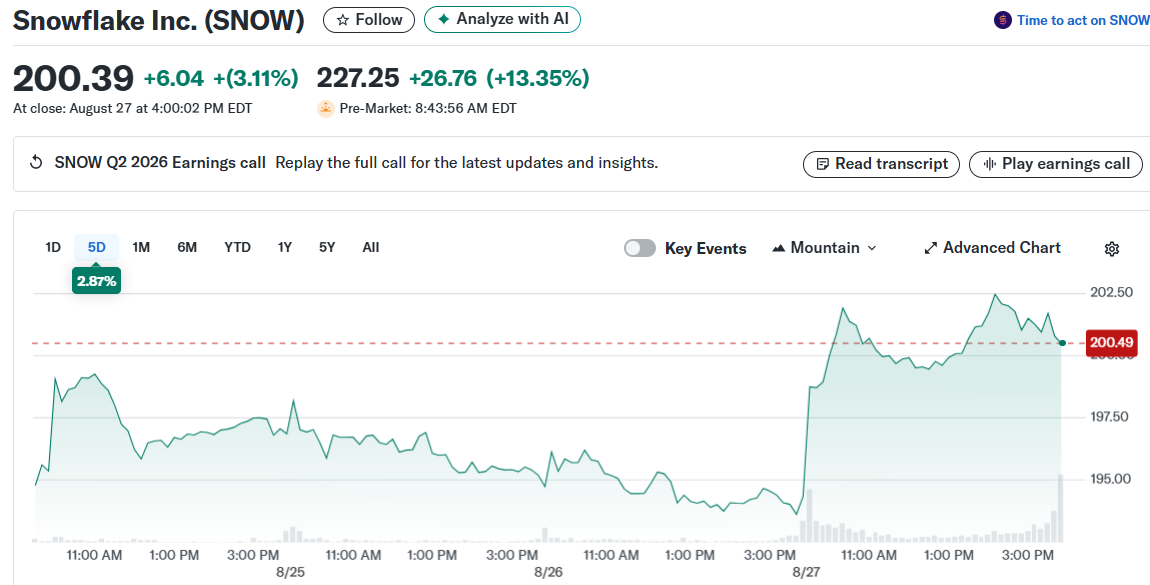

Snowflake stock exploded higher Thursday after the cloud data platform crushed second-quarter earnings expectations. Shares surged 14% in premarket trading following the strong results.

The company reported adjusted earnings of 35 cents per share on revenue of $1.14 billion. Wall Street had expected just 27 cents per share on $1.09 billion revenue.

The earnings beat reflects surging demand for Snowflake’s AI-powered database solutions. Companies are rapidly modernizing data infrastructure to support artificial intelligence initiatives.

“We have an enormous opportunity ahead as we continue to empower every enterprise to achieve its full potential through data and AI,” CEO Sridhar Ramaswamy said.

Raised Guidance Signals Strong Demand

Snowflake lifted its full-year outlook following the impressive quarter. The company now expects 2025 product revenue of $4.4 billion, up from its previous $4.33 billion estimate.

Third-quarter revenue guidance came in at $1.124-$1.13 billion versus the $1.121 billion Wall Street consensus. The raised forecasts suggest management sees continued AI-driven growth ahead.

The company reported particularly strong momentum on Microsoft Azure. Cloud usage surged across Europe, the Middle East, and Africa regions.

Snowflake’s premarket gains would add over $11 billion to its current $67 billion market capitalization if sustained.

Analyst Price Target Increases

Multiple Wall Street firms raised Snowflake price targets after the earnings beat. Evercore ISI analyst Kirk Materne boosted his target to $280 from $240.

“The combination of accelerating revenue growth and operating margin leverage can drive further multiple expansion,” Materne wrote while maintaining his Outperform rating.

BTIG’s Gray Powell increased his price target to $276 from $235. He called the results “exceptional” and sees Snowflake as “a clear beneficiary of AI as companies work to centralize their data.”

D.A. Davidson maintains a Buy rating with a $250 target, dismissing competition concerns despite rival Databricks’ recent $100 billion valuation.

Snowflake trades at 142.52 times earnings, higher than competitors MongoDB (75.76x) and Datadog (63.71x). The premium valuation reflects investor confidence in the company’s AI positioning.

The stock has gained 30% year-to-date as AI infrastructure spending accelerates. Nvidia’s recent strong forecast has boosted confidence across the entire AI ecosystem.

Richard Clode at Janus Henderson sees Snowflake benefiting from the next-generation database transition. The fund manager owns Snowflake shares and views it as well-positioned for continued AI growth.

Azure’s international expansion and enterprise AI adoption continue driving Snowflake’s revenue acceleration in the competitive cloud data market.

Get 3 Free Stock Ebooks

Discover top-performing stocks in AI, Crypto, and Technology with expert analysis.

- Top 10 AI Stocks - Leading AI companies

- Top 10 Crypto Stocks - Blockchain leaders

- Top 10 Tech Stocks - Tech giants