Stock: Revenue Rockets 217% But Losses Double in Q2")

TLDR

- SoundHound AI reported record Q2 revenue of $43 million, up 217% year-over-year

- Company raised full-year 2025 revenue guidance to $160-178 million range

- Net losses doubled to approximately $75 million compared to same period last year

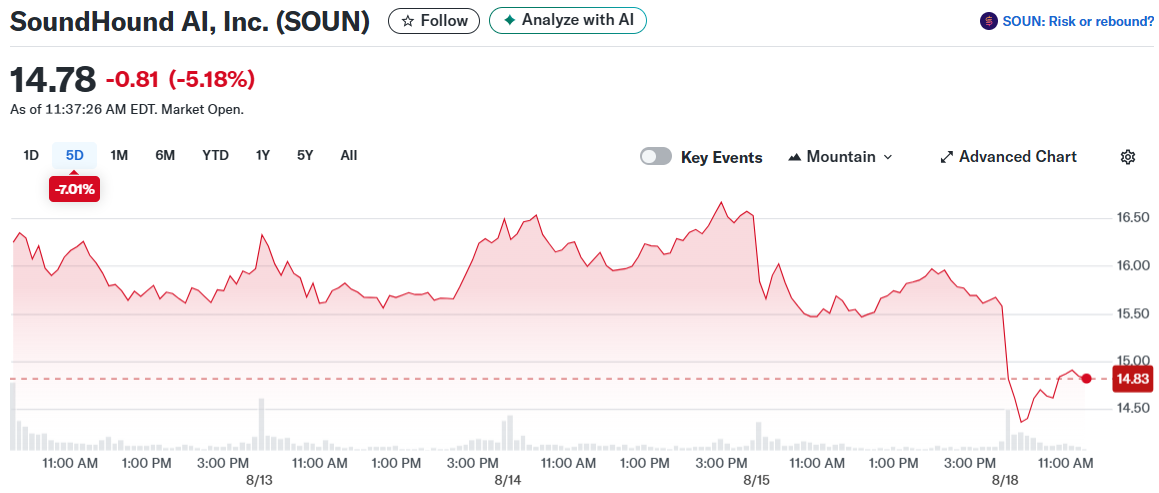

- Stock trades at $14.84, down from 52-week high of $24.98

- Wall Street analysts rate the stock as “Strong Buy” with average price target of $14.29

SoundHound AI delivered its strongest quarter in company history with Q2 revenue hitting $43 million. The 217% year-over-year growth rate stands out in today’s market environment.

The revenue surge came from multiple business segments. Automotive AI, enterprise customer service, and restaurant automation all contributed to the growth.

SoundHound’s Polaris foundation model drove much of this success. The multimodal, multilingual AI platform represents 20 years of research and development work.

Customers migrating to Polaris see immediate improvements in speed and accuracy. This leads to higher renewal rates and faster deal closures according to management.

The company launched Amelia 7 in May, its agentic AI platform powered by Polaris. Fifteen large enterprise customers have already made the switch to the new system.

Strong Growth, Growing Losses

Despite the revenue wins, SoundHound’s financial picture shows some red flags. Net losses doubled to around $75 million compared to the previous year.

Gross margins dropped sharply from 63% to 39%. The Amelia acquisition boosted revenue but hurt profitability margins.

The company posted an adjusted net loss of $0.03 per share. That’s actually an improvement from the $0.04 loss in the same quarter last year.

Adjusted EBITDA loss came in at $14.3 million. Management expects to reach adjusted EBITDA profitability by the end of 2025.

SoundHound ended Q2 with $230 million in cash and no debt. This gives the company runway to continue its growth investments.

Market Performance and Outlook

The stock currently trades at $14.84, down 4.84% on the day. The 52-week range spans from $4.33 to $24.98.

SoundHound raised its full-year 2025 revenue guidance. The new range of $160-178 million aligns with analyst consensus of $166 million.

Wall Street expects revenue to grow another 29.1% in 2026. The stock trades at 30 times forward sales, reflecting high growth expectations.

Five of seven analysts rate SOUN as “Strong Buy” while two suggest “Hold.” The average price target sits at $14.29.

The highest analyst target of $18 implies 12.1% upside potential. Recent analyst upgrades helped drive the stock higher in early August.

SoundHound launched Vision AI in August, expanding into real-time visual understanding. This adds to the company’s conversational AI capabilities.

The company struck partnerships with major automotive brands and restaurant chains. These deals should help drive future revenue growth across key verticals.

Get 3 Free Stock Ebooks

Discover top-performing stocks in AI, Crypto, and Technology with expert analysis.

- Top 10 AI Stocks - Leading AI companies

- Top 10 Crypto Stocks - Blockchain leaders

- Top 10 Tech Stocks - Tech giants