Stock: Revenue Soars But Investors Head for the Exits")

TLDR

- SoundHound AI reported 217% revenue growth in Q2 2025, raising full-year outlook to $169 million

- Stock dropped 6.47% Wednesday as AI sector faced selling pressure following bubble concerns

- Company trades at 46 times sales despite posting $74.7 million net loss in Q2

- Platform deployed in restaurants, automotive, healthcare, and financial services with seven of top 10 global banks as clients

- Wall Street projects 29% growth for 2026, down from current triple-digit expansion rates

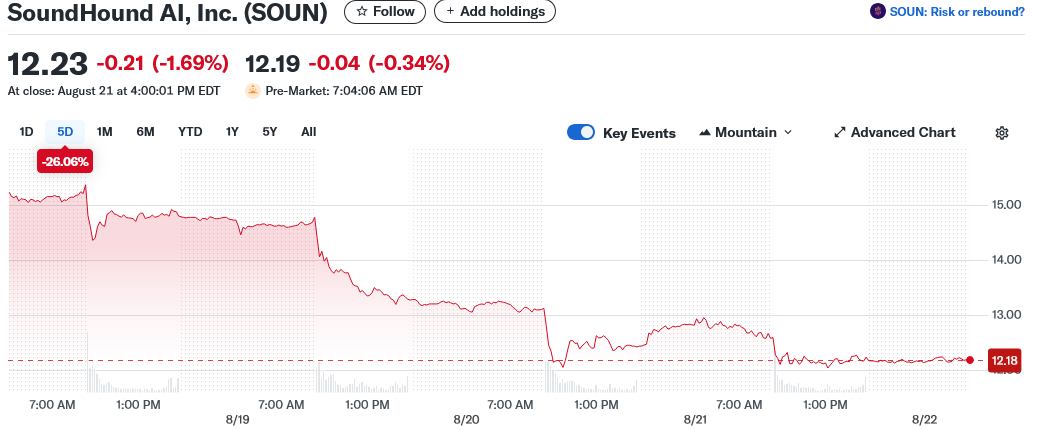

SoundHound AI stock extended its losing streak to four consecutive days this week, dropping 6.47% to close at $12.44 per share Wednesday. The decline came as investors pulled back from AI investments following industry bubble warnings.

The sell-off occurred across multiple AI companies after comments about bubble formation in the sector. This mirrors concerns about overvaluation that have plagued high-growth technology stocks.

Despite market pressure, SoundHound delivered impressive financial results in its recent quarterly report. Revenue jumped 217% year-over-year in the second quarter to $42.68 million, compared to $13.46 million in the same period last year.

The company also raised its full-year revenue outlook. Management increased guidance from approximately $167 million to $169 million for 2025.

SoundHound’s voice recognition technology represents an evolution beyond traditional assistants like Siri and Alexa. The platform has shown performance that exceeds human capabilities in certain applications.

Expanding Market Reach

The company has built partnerships across multiple industries. Its technology is deployed in restaurant chains and automotive systems, with expansion into healthcare and financial services underway.

Financial services adoption has been particularly strong. Seven of the world’s top 10 global financial institutions now use SoundHound’s platform for customer interactions.

Restaurant and automotive remain core markets. The voice recognition system handles complex orders and commands in these environments.

Healthcare applications are still developing. The company sees opportunities for voice-enabled medical record systems and patient interaction tools.

Revenue growth came with continued losses. The company posted a $74.7 million net loss in Q2, representing a 100% increase from the $37.3 million loss in the same quarter last year.

Operating losses reached $78 million in the quarter. This nearly doubled the $43 million in revenue generated during the same period.

Valuation Concerns Mount

The stock trades at 46 times sales, well above typical software company multiples. Most software companies trade between 10 and 20 times sales, though few are growing at SoundHound’s pace.

Wall Street analysts project slower growth ahead. Revenue growth is expected to moderate to 29% for 2026, down from current triple-digit rates.

The company has made multiple acquisitions recently. This makes it difficult to separate organic growth from purchased revenue expansion.

High valuations create pressure for continued execution. The stock price already reflects expectations for strong future performance.

Profitability remains elusive in the near term. The company prioritizes market share capture over immediate profit generation.

Competition in voice AI continues to intensify. Larger technology companies are developing competing solutions with substantial resources.

SoundHound’s current financial position shows cash burn exceeding revenue generation. This pattern is common among high-growth AI companies but creates timing pressure for reaching profitability.

The company raised its 2025 revenue guidance to $169 million, up from previous estimates of $167 million.

Get 3 Free Stock Ebooks

Discover top-performing stocks in AI, Crypto, and Technology with expert analysis.

- Top 10 AI Stocks - Leading AI companies

- Top 10 Crypto Stocks - Blockchain leaders

- Top 10 Tech Stocks - Tech giants