Stock: Voice AI Pioneer Surges 40% on Strong Earnings")

TLDR

- SoundHound AI stock jumped 26% in August after Q2 earnings beat with $42.7M revenue vs $32.9M expected

- Revenue growth of 217% year-over-year powered by voice AI technology adoption

- September rally continues with 14.3% gains following $60M Interactions acquisition

- DA Davidson raises price target to $17 from $15 on enterprise expansion strategy

- Full-year revenue guidance increased to $160M-$178M range

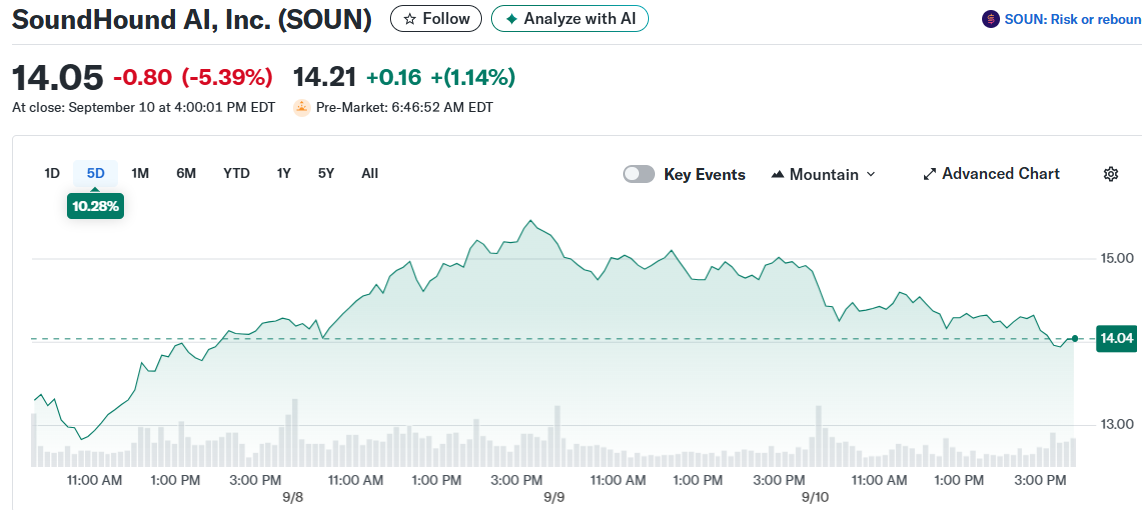

SoundHound AI has delivered explosive returns for investors over the past two months. The voice artificial intelligence company’s stock surged 26% in August and has added another 14.3% in September trading.

The rally began with SoundHound’s blockbuster Q2 earnings report on August 7th. The company smashed Wall Street expectations across key metrics.

Revenue came in at $42.7 million, crushing analyst estimates of $32.9 million. The earnings per share loss of $0.03 also beat forecasts of a $0.05 loss. Most impressive was the 217% year-over-year revenue growth rate.

Strong Fundamentals Drive Analyst Upgrades

Multiple investment firms upgraded SoundHound following the earnings release. The combination of revenue beats and growth acceleration caught Wall Street’s attention.

Some volatility emerged mid-August when an MIT study suggested most businesses haven’t achieved AI profitability yet. Rising inflation concerns also created temporary headwinds.

However, SoundHound stock quickly recovered as broader tech momentum returned. Federal Reserve interest rate cut expectations have supported AI stocks throughout September.

Strategic Acquisition Fuels Continued Rally

SoundHound announced its acquisition of Interactions for approximately $60 million in cash during September. Interactions specializes in enterprise voice AI solutions and brings established corporate relationships.

DA Davidson responded by raising their price target from $15 to $17 while maintaining a Buy rating. The firm believes the deal will immediately improve SoundHound’s margins and market position.

The acquisition aligns with SoundHound’s enterprise expansion strategy. Interactions’ client base provides access to major corporate accounts that can drive future growth.

Revenue Growth Trajectory Remains Strong

Management raised full-year revenue guidance to $160-178 million after the strong Q2 performance. Hitting the midpoint would represent 99.5% annual growth compared to 2023’s $84.7 million.

SoundHound’s technology spans automotive, smart devices, and customer service applications. The company has maintained efficient scaling while expanding its customer footprint.

The stock trades at 36.4 times expected sales, reflecting growth expectations. However, the consistent revenue acceleration suggests the premium valuation may be justified.

Recent partnerships and product launches continue building SoundHound’s competitive moat in conversational AI. The company recorded 85% revenue growth in 2024, establishing a track record of strong execution.

Get 3 Free Stock Ebooks

Discover top-performing stocks in AI, Crypto, and Technology with expert analysis.

- Top 10 AI Stocks - Leading AI companies

- Top 10 Crypto Stocks - Blockchain leaders

- Top 10 Tech Stocks - Tech giants