Stock: Pump and Dump Claims After First-Day NYSE Slide")

TLDRs;

- StubHub raised $800M in its IPO at $23.50 per share, but stock closed 4% lower on its first day.

- CEO Eric Baker remains in charge after regaining the company through Viagogo’s $4.05B deal in 2020.

- Revenue growth slowed to 3% in H1 2025, raising concerns after a 29% surge in 2024.

- StubHub faces lawsuits and probes over hidden fees, as consumer frustration with rising ticket prices grows.

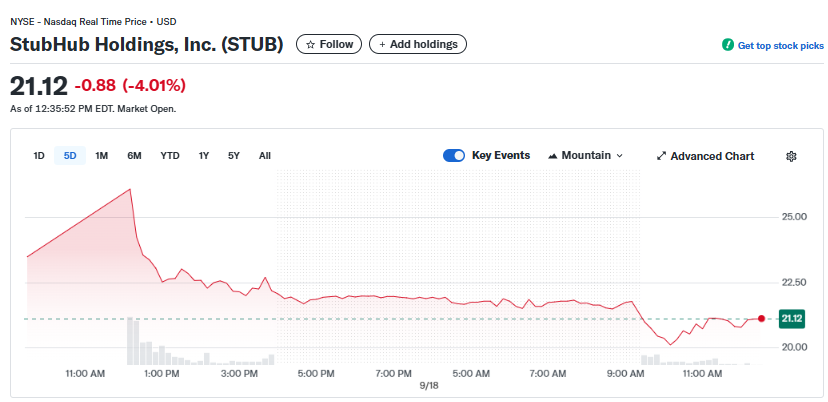

StubHub Holdings Inc. entered public markets Wednesday with a splash of excitement, but the cheers quickly faded as shares fell sharply on their first day of trading.

The ticket marketplace priced its long-awaited initial public offering (IPO) at $23.50 per share, only to see the stock tumble 4% by the close of trading, igniting speculation of a “pump and dump” style exit by early backers.

The New York-based firm raised about $800 million by selling just over 34 million shares. While the IPO gave StubHub an initial market capitalization in the range of $8.6 billion to $8.8 billion, the closing price dragged its valuation down closer to $8.1 billion. The ticker symbol “STUB” now sits under scrutiny from investors wondering whether the early hype justified the outcome.

Company History and CEO’s Role

Founded in 2000 by Eric Baker, StubHub has grown into one of the largest secondary ticket resale platforms globally. Its history is full of corporate twists, eBay purchased the platform in 2007, Baker left before that sale, and later launched the international rival Viagogo in 2006.

In 2020, eBay sold StubHub back to Viagogo for $4.05 billion, reuniting Baker with his original venture. Today, Baker retains his role as CEO and remains firmly in control.

StubHub’s competitors include SeatGeek and Vivid Seats, but the company boasts an enormous reach, with 40 million tickets sold in 2024 across more than 200 countries and territories. Despite that scale, the IPO slump hints at investor caution around profitability and regulatory pressures.

Financial Picture Raises Questions

StubHub’s growth trajectory has slowed. After posting a robust 29% revenue increase in 2024, the company reported only a 3% gain in the first half of 2025, with $827 million in sales.

Such deceleration may have dampened enthusiasm among investors hoping for faster expansion.

Meanwhile, the proceeds from the IPO will be used to pay down debt and cover general corporate purposes, according to company filings. That pragmatic use of funds has left some investors questioning whether fresh capital will go toward innovation or simply balance-sheet repairs.

Industry Challenges and Legal Scrutiny

Beyond financial performance, StubHub faces mounting regulatory heat. Authorities in Washington, D.C., New York, and Pennsylvania have all launched inquiries into hidden fees and misleading pricing practices.

In 2024, the D.C. attorney general sued the company for advertising deceptively low prices before tacking on steep service charges at checkout.

The ticketing industry as a whole is under fire as concert and sporting event prices continue to soar. According to U.S. Labor Department data, ticket prices rose 6.8% in 2023 and another 5.2% in 2024, outpacing inflation. That upward spiral has fueled consumer frustration and heightened calls for regulation.

A Cautionary IPO in a Hot Market

StubHub’s stumble comes during a surprisingly active year for IPOs, marking the strongest market since 2021. High-profile debuts have included Klarna, Figma, Circle Internet Group, and crypto exchange Gemini.

While some, like Klarna, saw double-digit first-day gains, StubHub’s reversal stands out as a cautionary tale: hype does not guarantee success.

Whether Wednesday’s slide was simply a typical market adjustment or a “pump and dump” exit by opportunistic early investors remains open to interpretation. But for StubHub, the challenge is clear, restore investor confidence while tackling slowing growth and regulatory scrutiny.

Get 3 Free Stock Ebooks

Discover top-performing stocks in AI, Crypto, and Technology with expert analysis.

- Top 10 AI Stocks - Leading AI companies

- Top 10 Crypto Stocks - Blockchain leaders

- Top 10 Tech Stocks - Tech giants