Stock: Plunges 34% on China Trade Restrictions and Earnings Miss")

TLDR

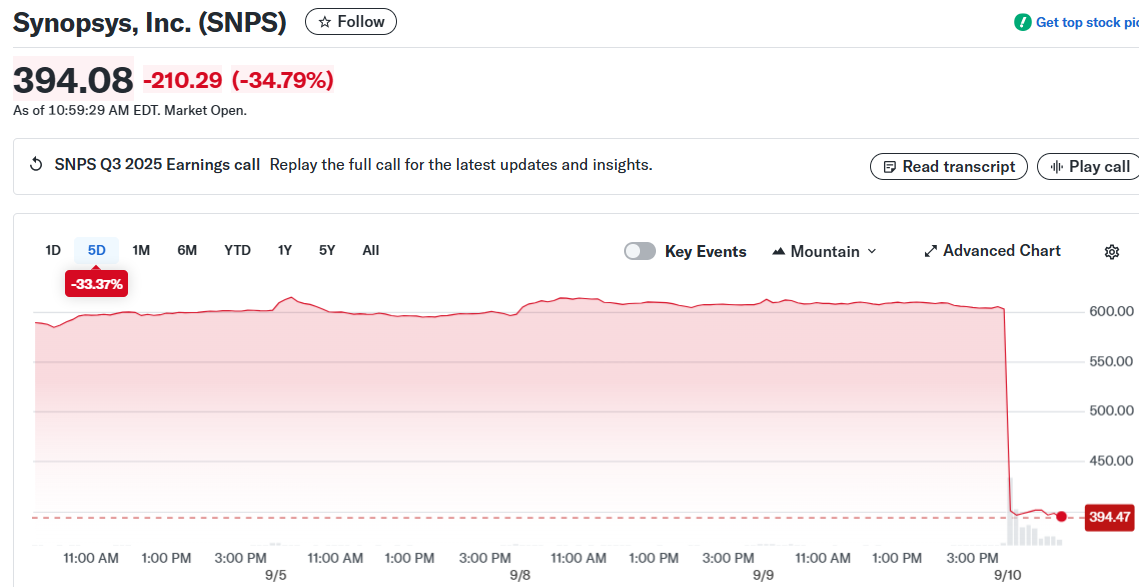

- Synopsys (SNPS) stock fell 34% on Wednesday, its worst decline in over three decades

- Company missed Q3 earnings expectations with $3.39 per share vs $3.80 expected

- US export restrictions disrupted business in China, hurting the IP division with 8% revenue drop

- CEO announced 10% workforce reduction and refocusing resources away from underperforming areas

- Analysts downgraded the stock citing poor outlook and challenges with major foundry customer likely Intel

Synopsys stock crashed 34% on Wednesday following a disappointing third-quarter earnings report that highlighted how US-China trade tensions are hurting the chip design software maker’s business. The decline marked the company’s worst single-day drop in more than three decades.

The Mountain View-based company reported adjusted earnings of $3.39 per share, falling short of the $3.80 analysts expected. Revenue came in at $1.74 billion, below the $1.77 billion Wall Street forecast.

CEO Sassine Ghazi pointed to multiple factors behind the weak performance. The company’s semiconductor intellectual property business saw an 8% revenue decline during the quarter.

“We had the expectation of deals that did not materialize,” Ghazi explained during the earnings call. He cited US export restrictions that disrupted design projects in China as a primary factor.

The export controls have compounded existing weakness in China, which represents the world’s largest semiconductor market. These restrictions are part of ongoing US government efforts to limit Chinese access to advanced chip technology.

Ghazi also mentioned challenges with a major foundry customer that will continue affecting results for the remainder of the year. Baird analysts believe this customer is likely Intel, given Synopsys’ longstanding partnership with the chipmaker.

Workforce Cuts and Strategic Shifts

The company announced plans to reduce its workforce by about 10% as part of a strategic refocus. Ghazi said the company would be reallocating resources away from areas that haven’t delivered expected returns.

“We made certain road map and resource decisions that did not yield their intended results,” the CEO admitted. The company is now pivoting to concentrate on more promising opportunities.

Synopsys shares had gained 25% year-to-date through Tuesday’s close before Wednesday’s massive selloff. The stock traded at $401.50 in morning trading, representing a dramatic reversal of fortune for the chip design software leader.

Analyst Downgrades Follow Poor Results

The disappointing results prompted immediate analyst downgrades. Baird downgraded Synopsys from Buy to Neutral, citing the below-consensus outlook and weak expectations for intellectual property growth in fiscal 2026.

“It is not our preference to downgrade stocks into weakness, but this update and lack of forward visibility create overhang that likely takes time to clear,” Baird analysts wrote. They acknowledged Synopsys remains an elite franchise but noted the current challenges.

BofA Securities took an even more bearish stance, double-downgrading the stock from Buy to Underperform. The firm slashed its price target to $525 from $625.

BofA analysts argued the headwinds are company-specific since Synopsys relies more heavily on IP revenue compared to rival Cadence Design Systems. Cadence stock fell 7% on Wednesday but remained BofA’s top pick in the sector.

For the current quarter ending October 31, Synopsys guided for adjusted earnings of $2.78 per share on revenue of $2.25 billion. This compares to analyst expectations of $4.50 per share on $2.01 billion in sales.

The company did see some bright spots, with its design automation segment growing 23% year-over-year. This growth included a $77 million contribution from Ansys, the simulation company Synopsys acquired earlier this year.

Get 3 Free Stock Ebooks

Discover top-performing stocks in AI, Crypto, and Technology with expert analysis.

- Top 10 AI Stocks - Leading AI companies

- Top 10 Crypto Stocks - Blockchain leaders

- Top 10 Tech Stocks - Tech giants