TLDR:

- Nvidia shares rose over 3% in pre-market trading ahead of its Q1 earnings report.

- Investors are closely watching the impact of U.S. export restrictions on Nvidia’s China sales.

- The company faces pressure on gross margins due to $5.5 billion in expected charges from export curbs.

- Market optimism tempered by concerns over future guidance and competitive challenges in AI chip markets.

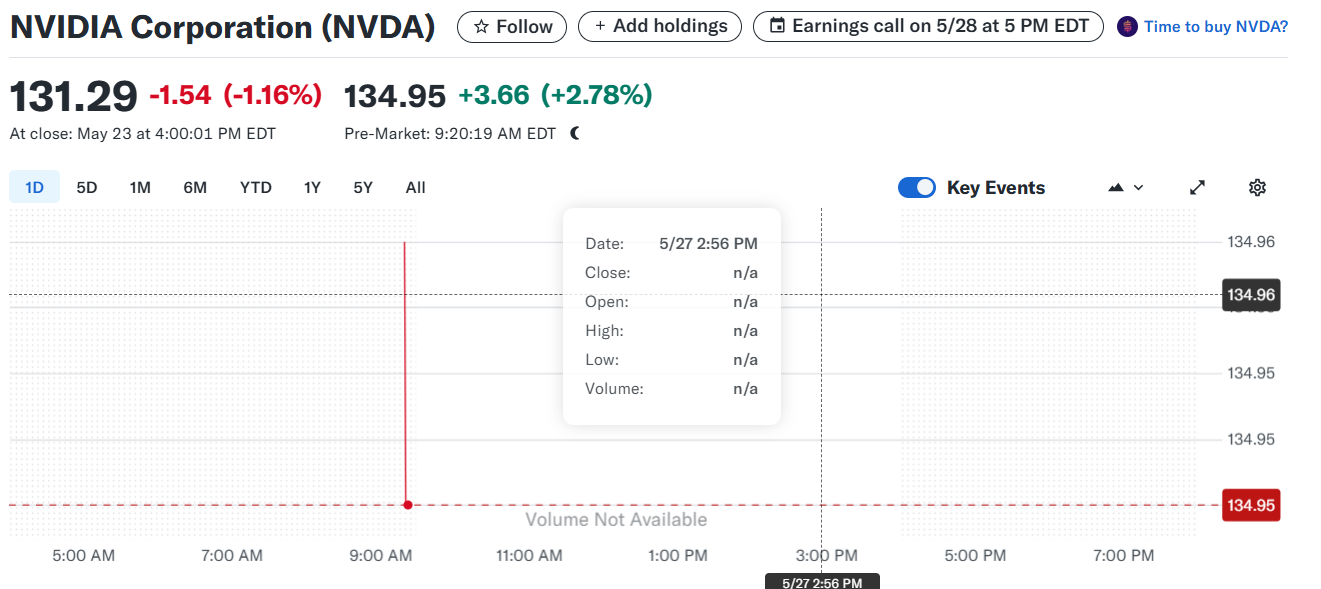

Nvidia Corp. (NVDA) a global leader in semiconductor technology, saw its stock climb just over 3% in pre-market trading on Tuesday ahead of its highly anticipated first-quarter earnings report scheduled for release on May 28.

NVDA Soars

At 9.19 AM EDT, Nvidia shares were trading at approximately $134.94, up $3.69 or 2.79% from the previous close. The pre-market gains mirrored a broader rally in U.S. stock futures, with major indices such as the S&P 500, Nasdaq 100, and Dow Jones futures all rising by over 1.5%.

Investors are eager for insights on how Nvidia is navigating the evolving market conditions, particularly in light of recent geopolitical and regulatory challenges.

China Export Curbs Cast Shadow Over Earnings

A major focus for the upcoming earnings report is the impact of U.S. export restrictions on Nvidia’s business in China. Last month, the Trump administration imposed limits on the company’s ability to sell its advanced H20 AI chip to Chinese customers. Nvidia has indicated that these restrictions could lead to charges totaling $5.5 billion in the quarter, reflecting lost revenue and inventory write-downs.

Last week, CEO Jensen Huang revealed that Nvidia has walked away from $15 billion in potential sales in China, a market that accounted for roughly 13% of the company’s revenue last year. While Nvidia has begun developing a new AI chipset compliant with the export rules, uncertainty about its future China sales remains a key concern for investors. Analysts estimate the quarterly revenue hit from these curbs could be between $3 billion and $4.5 billion, with significant margin pressure expected.

Market Expectations

The restrictions on China-bound chips are expected to weigh heavily on Nvidia’s gross margins. Estimates suggest an adjusted gross margin drop of more than 11 percentage points to around 67.7%, with the H20-related write-offs potentially accounting for a margin reduction of up to 12.5%. This represents a sharp decline from Nvidia’s previously strong margin performance.

Despite the challenges, Nvidia is still forecasted to report robust revenue growth, with first-quarter sales expected to surge over 66% year-over-year to approximately $43.3 billion. However, Wall Street’s expectations appear more cautious compared to past quarters, reflecting a more tempered outlook given geopolitical headwinds and rising AI infrastructure costs.

Is $NVDA a buy ahead of earnings?

Nvidia reports May 28 with record revenue expected ($43.3B), but faces a $5.5B China write-off, slowing AI spend, and rising competition.

YTD shares are down ~5%. Data center growth and Blackwell chip momentum are key—but geopolitical risks…

— Dividend.com (@dividenddotcom) May 27, 2025

Future Outlook

While the China export curbs present a significant hurdle, Nvidia is simultaneously eyeing opportunities in new regions. Recent easing of U.S. export controls, specifically the modification of the AI diffusion rule—may open doors in markets such as the Middle East. Nvidia has already committed to selling large volumes of AI chips to countries like Saudi Arabia, supported by government trade agreements.

Industry analysts remain optimistic about Nvidia’s long-term position as a dominant player in AI technology, although some caution that the days of dramatic earnings beats may be over.

Get 3 Free Stock Ebooks

Discover top-performing stocks in AI, Crypto, and Technology with expert analysis.

- Top 10 AI Stocks - Leading AI companies

- Top 10 Crypto Stocks - Blockchain leaders

- Top 10 Tech Stocks - Tech giants