Stock: Soars on Double-Digit Dividend, Buyback Supports Holiday Momentum")

TLDRs:

- Tesco shares hit a 52-week high, boosted by dividend increase and share buyback program.

- UK grocery inflation eases to 4.7%, supporting festive promotions and investor optimism.

- Tesco sales rise 5.9% over 12 weeks, with market share reaching 28.2% amid competition.

- Share buybacks and capital returns support EPS while margins may face holiday pressure.

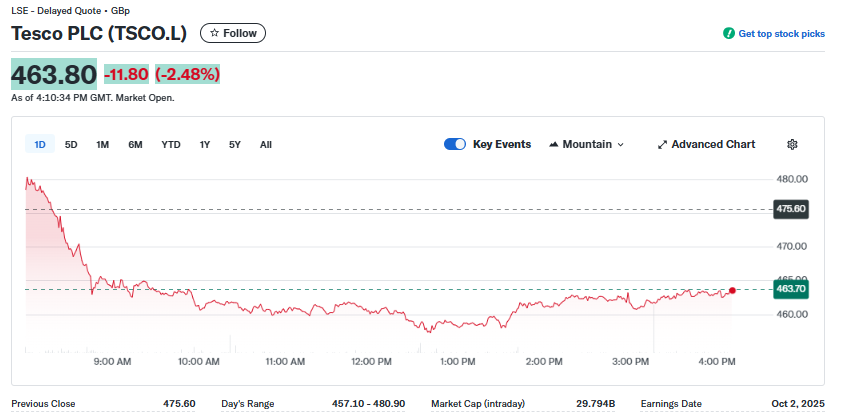

Tesco (LSE: TSCO) opened at 480.00p on 11 November 2025, briefly reaching a fresh 52-week high of 480.50p before slipping back to trade in the 464 range, a 2.35% drop, by early afternoon.

The previous close had been 475.60p, marking an intraday swing of nearly 3–4%. Analysts attribute the volatility to profit-taking following a strong run and sector headlines highlighting heavy festive promotions.

The day’s trading range of 457.30–480.50p underscores both the enthusiasm around Tesco’s capital returns and the caution investors are showing amid seasonal uncertainty.

Dividend and Buyback Drive Investor Interest

Tesco recently announced a double-digit dividend increase alongside an active £1.45bn share buyback program, of which approximately £1.10bn had already been executed by 7 November.

The buyback reduces the company’s share count, supporting earnings per share, while the enhanced dividend signals confidence in both short- and medium-term profitability.

With the interim dividend scheduled for 21 November, income-focused investors are taking note, particularly as the company enters its busiest trading period of the year.

Market Share and Sales Momentum

Over the 12 weeks ending 2 November, Tesco reported a 5.9% rise in sales, with market share climbing to 28.2%.

Comparatively, Ocado recorded 15.9% sales growth, while Lidl maintained double-digit growth of 10.8% in bricks-and-mortar sales. Industry coverage highlights Tesco and Lidl as leading the pack, reinforcing the competitive pressure shaping holiday pricing.

Analysts suggest Tesco’s scale, loyalty programs such as Clubcard Prices, and supplier relationships allow it to maintain market share while managing margin pressures more effectively than smaller rivals.

While UK grocery inflation cooled to 4.7% in the four weeks to 2 November, promotional spending surged 9.4% year-over-year, compared with only 1.8% growth on full-price items.

The heavier promotional mix is expected to support store traffic and volume, but could squeeze gross margins if discounting intensifies. Tesco’s management has flagged this dynamic, noting confidence in festive trading while maintaining vigilance on profit efficiency. Investors are closely watching how the interplay between promotional intensity, market share, and margin management will play out in the coming weeks.

Strategic Outlook into Christmas

Tesco had already raised its FY25/26 adjusted operating profit guidance to £2.9–3.1bn, citing resilient demand and market share gains.

With the share buyback steadily shrinking the float, the company is positioned to deliver capital returns while supporting stock performance. Key considerations for investors heading into the holidays include ongoing promotional strategies, market share cadence against discount rivals, macroeconomic influences such as UK rate cuts and consumer confidence, and the trajectory of Tesco’s buyback program into 2026.

In summary, 11 November 2025 highlights both technical and fundamental dynamics: a record-high surge tempered by intraday profit-taking, alongside a strong underlying business supported by easing inflation, rising sales, and ongoing shareholder returns. The coming weeks will test how much of the festive season resilience is already priced in and how Tesco balances growth with margin discipline during peak trading.

Get 3 Free Stock Ebooks

Discover top-performing stocks in AI, Crypto, and Technology with expert analysis.

- Top 10 AI Stocks - Leading AI companies

- Top 10 Crypto Stocks - Blockchain leaders

- Top 10 Tech Stocks - Tech giants