Stock: Why This New China Model Could Change Everything")

TLDR

- Tesla launches six-seat Model Y L in China for RMB 339,000 targeting family buyers

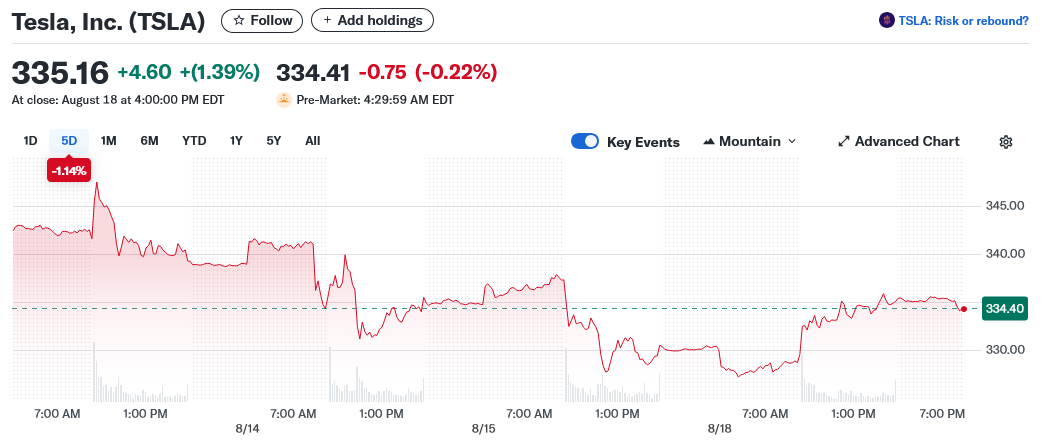

- Stock trades at $335.16, up 1.4% with technical indicators suggesting potential breakout

- Investor Bay Area Ideas downgrades to Hold despite long-term growth potential

- Tesla board awards Musk $30 billion compensation package to retain CEO

- Stock faces resistance at $348-$350 with September deliveries key catalyst

Tesla stock climbed 1.4% to $335.16 as the electric vehicle maker unveiled its new six-seat Model Y L variant in China. The launch represents a strategic push into the family EV segment where Tesla has traditionally struggled.

The Model Y L carries a price tag of RMB 339,000, roughly $47,180. It sits between the standard Model Y and Tesla’s more premium offerings.

What makes this version different is the extended wheelbase of 3,040 mm. The extra space addresses a longtime complaint about cramped third-row seating in previous Tesla models.

Deliveries are scheduled to begin in September. That timing aligns with China’s typical fourth-quarter sales surge.

Tesla faces intense competition in China from domestic brands like BYD, Li Auto, Nio, and XPeng. These companies have been gaining market share and often outpace Tesla in innovation cycles.

The Model Y L directly targets family buyers, a segment where competitors like the Zeekr 009 and Li Auto L9 have dominated. Tesla’s move appears calculated to stop further market erosion.

Technical Picture Shows Potential

From a technical standpoint, Tesla stock is approaching key resistance levels. The intraday high reached $336.22 with a low of $327.01.

Volume supports the recent upward movement with over 56 million shares traded. That figure suggests institutional interest is returning after a quiet July period.

The 200-day moving average now acts as support, giving bulls confidence. The Relative Strength Index remains moderate, indicating the stock isn’t overbought.

A decisive close above $348-$350 would strengthen the case for a rally toward $370-$380. Options activity shows increased positioning around $350 and $360 call strikes.

Mixed Views on Valuation

Not everyone is convinced Tesla’s current valuation makes sense. Investor Bay Area Ideas recently downgraded the stock to Hold despite believing in the long-term story.

“I believe Tesla shares are quite obviously overvalued relative to current financials,” the investor explained. However, they added that for patient investors who trust the growth story, “the valuation is not completely outrageous.”

The bull case hinges on advancements in robotaxis, affordable models, and autonomous ventures. These projects keep Tesla’s growth narrative alive despite near-term headwinds.

One major headwind is the removal of the $7,500 EV consumer tax credit expiring at the end of September. This could pressure demand in Tesla’s home market.

Tesla’s board recently approved a $30 billion stock-based compensation package for CEO Elon Musk. The decision aims to keep Musk focused on the company’s AI ambitions while a previous compensation deal works through the courts.

Bay Area Ideas called the package size “outrageous” but necessary. “If he were to leave Tesla, the long-term direction of sales and innovation could be negatively affected,” they noted.

Tesla shares have fallen 17% year-to-date despite the recent gains. Weakening year-over-year EV sales in both Q1 and Q2 2025 have weighed on performance.

The company trades at a premium to other automakers based on its robotics and robotaxi vision. Whether this premium is justified depends largely on execution of these future technologies.

Wall Street remains split on Tesla with 14 Buy ratings, 15 Holds, and 8 Sells. The consensus Hold rating reflects this uncertainty.

The 12-month average price target of $307.23 implies about 8% downside from current levels. This suggests analysts see limited upside in the near term.

The Model Y L’s reception in China will be crucial for Tesla’s next move. Strong pre-orders could provide the catalyst needed to break above resistance levels.

Get 3 Free Stock Ebooks

Discover top-performing stocks in AI, Crypto, and Technology with expert analysis.

- Top 10 AI Stocks - Leading AI companies

- Top 10 Crypto Stocks - Blockchain leaders

- Top 10 Tech Stocks - Tech giants