TLDR

- Nvidia reports quarterly earnings Wednesday with investors watching AI demand growth and China trade policy impacts

- Federal Reserve’s preferred inflation measure (PCE) releases Friday, could influence September rate cut decision

- Fed Chair Powell’s dovish Jackson Hole comments boosted rate cut expectations above 80% for September meeting

- Rate-sensitive sectors like homebuilders and banks rallied strongly on interest rate cut hopes

- Market rotation occurring from big tech stocks toward cyclical and value sectors

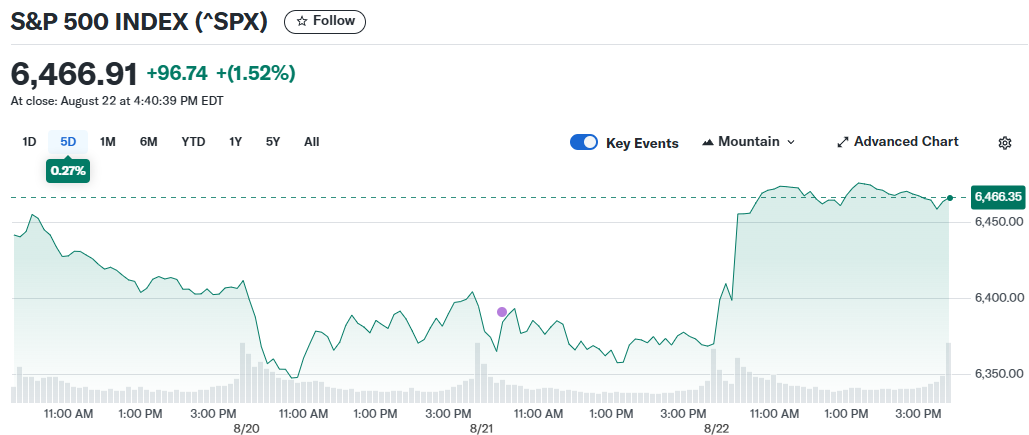

The US stock market prepares for a pivotal week as Nvidia earnings and key inflation data take center stage. Fed Chair Jerome Powell’s dovish remarks at Jackson Hole have already boosted investor sentiment and rate cut expectations.

Markets surged Friday after Powell signaled potential interest rate cuts in September. The Dow gained 1.5% while the S&P 500 rose 0.3%. Small-cap and cyclical sectors outperformed large-cap technology stocks in the rally.

Nvidia reports second-quarter earnings Wednesday in what analysts consider the week’s most important event. The AI chipmaker has driven much of the artificial intelligence boom through surging sales. Investors will scrutinize updates on the company’s most advanced product offerings.

The company faces headwinds from China export restrictions worth approximately $8 billion in lost revenue. Nvidia recently made a deal with the Trump administration to share revenue from AI chip sales in China. The chipmaker is also considering new products specifically for the Chinese market pending government approval.

Analysts expect Nvidia to post another sales record despite the China challenges. The company’s performance could indicate whether AI demand remains strong across global markets. Other technology companies reporting earnings include Dell, CrowdStrike, Snowflake, and Autodesk.

Rate Cut Expectations Drive Sector Rotation

September interest rate cut probability now exceeds 75% following Powell’s Jackson Hole speech. This dovish shift has sparked rotation from big tech stocks into rate-sensitive sectors. Homebuilders, banks, and small-cap companies rallied strongly on lower borrowing cost expectations.

The “Magnificent Seven” tech stocks rebounded Friday but face continued pressure from sector rotation. Cyclical and value sectors are showing outperformance as investors anticipate easier monetary policy. This trend could accelerate if inflation data supports Fed dovishness.

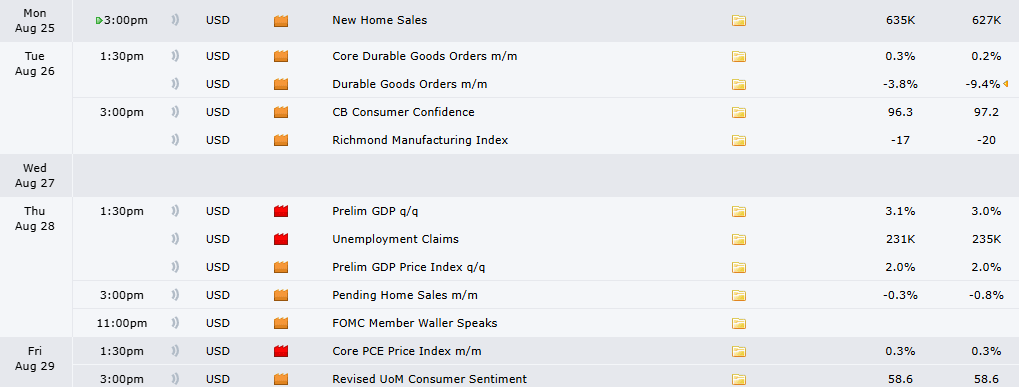

Consumer confidence data releases Tuesday along with durable goods orders for July. Richmond Fed President Tom Barkin will speak both Tuesday and Wednesday. These events could provide additional Fed policy clues before the September meeting.

Inflation Data Could Seal Rate Cut Decision

Friday’s Personal Consumption Expenditures (PCE) index represents the week’s other major catalyst. The PCE serves as the Federal Reserve’s preferred inflation measurement. July data could heavily influence the September rate decision timing and magnitude.

June PCE showed inflation ticked higher that month creating some Fed concerns. However, earlier July inflation reports indicated price increases were lower than feared. A benign PCE reading would likely cement September rate cut expectations.

Additional economic data includes new home sales Monday and pending home sales Thursday. Consumer sentiment surveys and trade balance figures round out the week’s economic calendar. GDP revisions for the second quarter also release Thursday.

The week brings earnings from several Canadian banks including Bank of Montreal and Royal Bank of Canada. Marvell Technology and PDD Holdings also report results. These earnings could provide insight into global economic conditions and consumer spending patterns.

Nvidia announced it expects growing revenue despite China export restriction challenges worth $8 billion in potential lost sales.

Get 3 Free Stock Ebooks

Discover top-performing stocks in AI, Crypto, and Technology with expert analysis.

- Top 10 AI Stocks - Leading AI companies

- Top 10 Crypto Stocks - Blockchain leaders

- Top 10 Tech Stocks - Tech giants