Stock: Faces Pressure Amid CoWoS Packaging Bottlenecks and AI Demand Surge")

TLDRs;

- TSMC’s October revenue rose 16.9% YoY, its slowest growth since February, as packaging constraints weigh on supply.

- TSM shares dip amid tightening CoWoS capacity and rising AI chip orders from Nvidia, AMD, and Apple.

- CoWoS utilization remains near 60%, with relief expected as new plants come online by 2026.

- Global AI spending projected to hit $400B by 2026, intensifying pressure on TSMC’s chip output and margins.

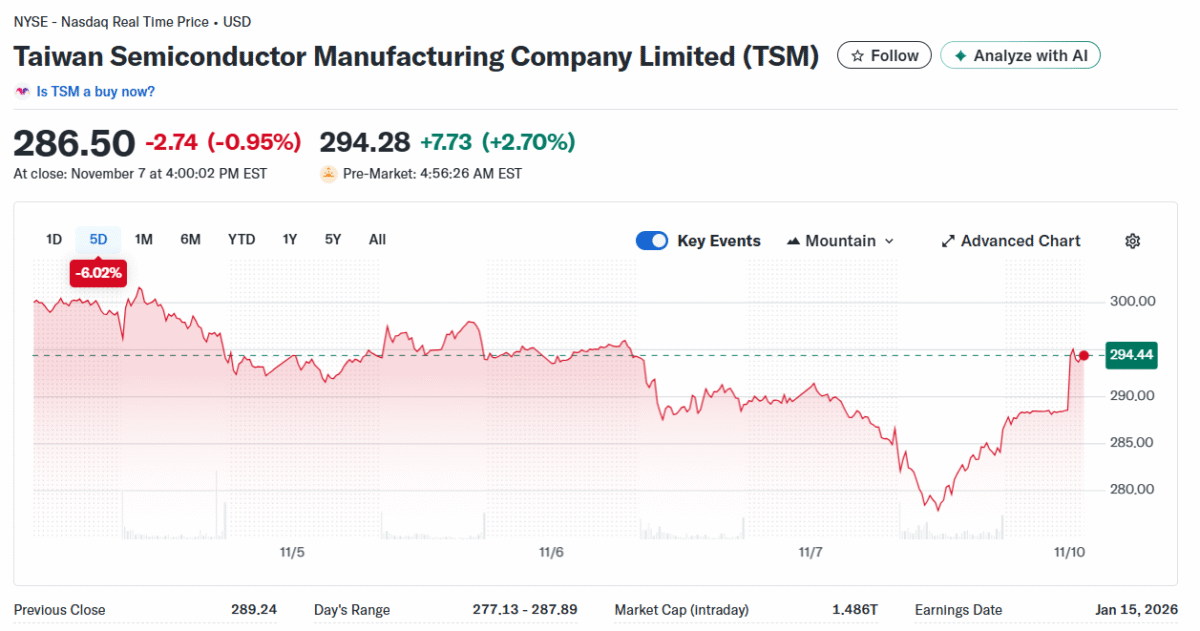

Taiwan Semiconductor Manufacturing Co. (TSMC) shares traded lower following the company’s October revenue update, reflecting investor concern over tightening production capacity and slower growth momentum.

The stock, listed on the NYSE under ticker symbol TSM, closed at $286.50, down 0.95% in the previous session, before rebounding 2.63% in pre-market trading Monday to $294.08.

TSMC reported a 16.9% year-on-year increase in October revenue, marking its slowest growth since February 2024. Still, analysts expect a rebound in the current quarter, projecting a 27.4% rise in sales, driven by sustained demand from Nvidia, AMD, Qualcomm, and Apple. The company’s stock remains up around 37% year-to-date, underscoring investor faith in its strategic position at the heart of the AI chip supply chain.

Despite the soft October performance, TSMC’s leadership reaffirmed confidence in its long-term trajectory. CEO C.C. Wei noted that the company’s advanced packaging capacity remains “very tight,” but expansion plans are well underway to meet surging demand from global AI chipmakers.

Packaging Bottlenecks Challenge AI Supply Chain

TSMC’s modest revenue growth isn’t a demand problem, it’s a supply constraint issue tied to the company’s Chip-on-Wafer-on-Substrate (CoWoS) packaging process. This advanced interconnect technology is essential for assembling AI GPUs, such as those designed by Nvidia, which rely on high-bandwidth memory and dense power integration.

Currently, CoWoS utilization sits near 60%, as new packaging tools ramp up slower than anticipated. TSMC plans to expand capacity to 70,000 wafers per month by late 2025 and 90,000 by the end of 2026, up from around 35,000 in 2024. Much of this growth will come from new facilities in Chiayi and the upcoming AP8 plant, both critical for easing the bottleneck.

This production squeeze has created a trickle-down effect across the AI hardware market. Nvidia, one of TSMC’s largest clients, is expected to secure nearly 60% of the global CoWoS wafer supply by 2026 to maintain its GPU dominance. That dynamic leaves smaller players like AMD and Qualcomm, jockeying for remaining capacity, further tightening supply through next year.

Memory Constraints Add to the Pressure

Alongside CoWoS bottlenecks, the industry is facing a high-bandwidth memory (HBM) shortage that’s reshaping pricing and profitability. Samsung Electronics announced that its 2026 HBM production is already fully booked, signaling continued scarcity across the ecosystem.

Server DRAM prices are projected to climb 18–23% in Q4 2025, driven by new data center expansions and rising AI inference workloads. Meanwhile, HBM3E prices could slip amid intensified competition, setting up a crossover in profitability by early 2026. This shift is pushing OEMs toward DDR5 and LPDDR5X alternatives to maintain cost efficiency.

System integrators are also exploring KVCache offloading, a memory optimization technique that uses traditional DRAM to store prior model states, an attractive option as HBM shortages persist. This adaptation underscores how downstream players are adjusting to upstream supply friction.

AI Spending Surge Keeps Long-Term Outlook Strong

Despite near-term production limits, TSMC’s long-term demand outlook remains robust. According to Bloomberg estimates, major U.S. tech firms are projected to spend over $400 billion on AI development by 2026, a 21% increase from 2025.

This exponential growth ensures that TSMC remains a central beneficiary of the AI infrastructure boom, even as it navigates temporary headwinds. For investors, the company’s challenge lies in managing capacity constraints without slowing innovation, a balancing act that will determine its performance heading into 2026.

Get 3 Free Stock Ebooks

Discover top-performing stocks in AI, Crypto, and Technology with expert analysis.

- Top 10 AI Stocks - Leading AI companies

- Top 10 Crypto Stocks - Blockchain leaders

- Top 10 Tech Stocks - Tech giants