Stock: Gene Therapy Results Drive 220% Weekly Rally")

TLDR

- uniQure (QURE) stock surged 220% this week after releasing positive Phase 1/2 results for AMT-130 Huntington’s disease gene therapy

- High-dose patients showed statistically significant 75% slowing of disease progression at 36 months versus control data

- Secondary endpoints included 60% slowing in functional capacity decline and stable neurodegeneration biomarkers

- Company targets FDA filing in Q1 2026 under accelerated approval pathway following Q4 2025 pre-BLA meeting

- Analysts raised price targets with Goldman modeling $2.5B peak sales and 90% success probability

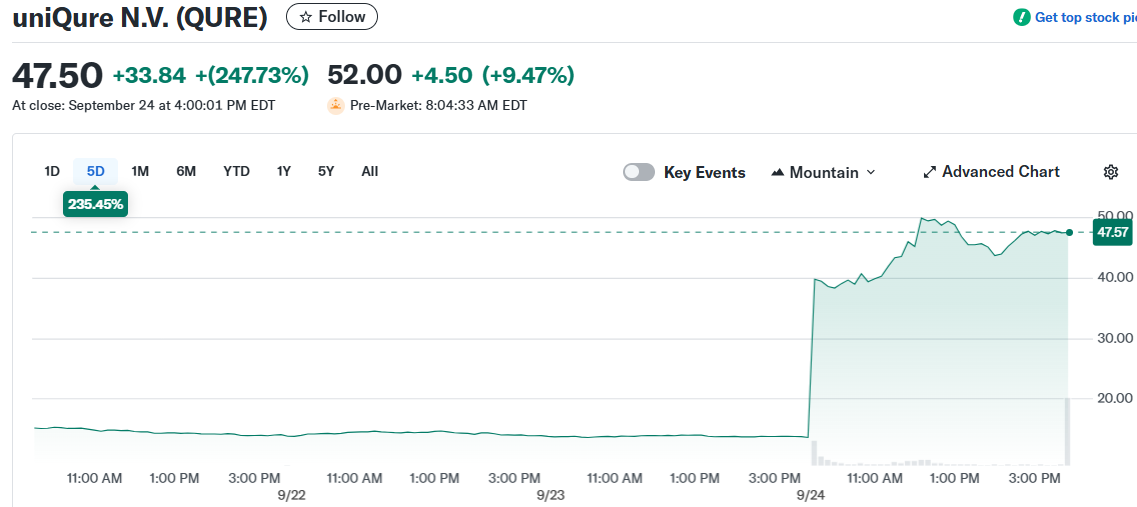

uniQure stock experienced explosive growth this week, rallying over 220% following positive clinical trial results for its Huntington’s disease treatment. The biotech company released topline data from its pivotal Phase 1/2 study of AMT-130 gene therapy.

The stock approached its 52-week high of $51.21 as trading volume surged well above the average 2.2 million shares. Investors responded enthusiastically to the three-year follow-up data from treated patients.

AMT-130 demonstrated statistically significant efficacy in the high-dose cohort. The therapy showed 75% mean slowing of disease progression using the composite Unified Huntington’s Disease Rating Scale compared to natural history controls.

Strong Secondary Endpoints Support Primary Data

The gene therapy also met key secondary measures. Patients experienced 60% slowing of disease progression in total functional capacity assessments at 36 months.

Cerebrospinal fluid neurofilament light protein levels remained below baseline throughout the study period. This biomarker indicates neurodegeneration and its stability suggests potential neuroprotective effects.

The safety profile remained consistent with previous releases. No new treatment-related serious adverse events occurred since December 2022.

uniQure plans FDA engagement in Q4 2025 through a pre-BLA meeting. The company will discuss regulatory requirements for its accelerated approval pathway submission.

Analyst Price Targets Rise on Clinical Success

Goldman Sachs maintained its Neutral rating with a $56 price target following the data announcement. The firm projects potential peak global sales of $2.5 billion for AMT-130.

Their analysis assumes 90% probability of regulatory success and 25% market penetration. Approximately 20,000 symptomatic patients are diagnosed in the United States.

Leerink Partners increased its price target to $68 from $48 while keeping an Outperform rating. The firm highlighted the clinical results as particularly strong data.

Stifel raised its target to $65 from $30, emphasizing potential U.S. market opportunity exceeding $1 billion by 2031. TD Cowen reiterated its Buy rating after the primary endpoint achievement.

The company announced a $200 million public offering of ordinary shares and pre-funded warrants. Leerink Partners, Stifel, Van Lanschot Kempen, and Guggenheim Securities serve as bookrunning managers.

uniQure targets BLA filing in Q1 2026 under the accelerated approval pathway based on current clinical data.

Get 3 Free Stock Ebooks

Discover top-performing stocks in AI, Crypto, and Technology with expert analysis.

- Top 10 AI Stocks - Leading AI companies

- Top 10 Crypto Stocks - Blockchain leaders

- Top 10 Tech Stocks - Tech giants