Stock: Climbs Higher as Cybersecurity Company Outperforms Nvidia in 2025")

TLDR

- Zscaler stock has surged 59% in 2025, significantly outpacing Nvidia’s 32% gain

- Revenue reached $2.7 billion in fiscal 2025, representing 23% year-over-year growth

- AI-focused cybersecurity solutions driving expansion with 85% growth in agentic security operations

- Remaining performance obligations jumped 31% to $5.8 billion, indicating strong future revenue

- Freedom Capital Markets upgraded stock to buy with $320 price target after strong Q4 results

Zscaler has become the surprise AI stock winner of 2025, delivering impressive returns that have left even Nvidia trailing behind. The cybersecurity specialist has posted a 59% stock price gain this year, compared to Nvidia’s 32% return.

The cloud-based security provider reported fiscal 2025 revenue of $2.7 billion, marking 23% growth from the previous year. This performance showcases how the company is capitalizing on the convergence of artificial intelligence and cybersecurity.

Zscaler specializes in zero-trust security solutions, which verify user and device identities before granting network access. The zero-trust security market is projected to reach $92 billion annually by 2030, growing at approximately 17% per year.

The company is expanding faster than its broader market category. Its strategy centers on providing cybersecurity tools specifically designed to protect AI applications, secure access to AI apps, and safeguard large language models.

AI Security Solutions Drive Revenue Growth

Zscaler’s AI-focused offerings are delivering exceptional results. The company’s agentic AI security operations recorded 85% annual recurring revenue growth year-over-year. Meanwhile, its agentic AI operations expanded by 58% during the same timeframe.

These solutions help organizations identify IT outages, implement corrective measures, and enhance troubleshooting processes. The agentic AI cybersecurity market is expected to grow at 34% annually through 2033, potentially generating $322 billion in revenue.

The company’s remaining performance obligations surged 31% to $5.8 billion in the latest quarter. This metric represents contracted future revenue and currently exceeds double Zscaler’s most recent annual revenue figure.

The accelerated growth in contracted backlog versus quarterly revenue indicates robust demand for services. This suggests Zscaler is securing new business faster than it can fulfill existing contracts.

Analyst Upgrades Follow Strong Quarter

Freedom Capital Markets analyst Almas Almaganbetov upgraded Zscaler to buy from hold this week. He increased his price target 14% to $320 per share following the company’s fiscal fourth-quarter earnings release.

The analyst highlighted broad-based growth across Zscaler’s product portfolio. Revenue climbed 21% year-over-year in Q4, while annual recurring revenue increased 22%. Calculated billings advanced 32% during the period.

Almaganbetov emphasized strong demand for Zscaler’s AI-enhanced solutions as a primary growth catalyst. He believes this demonstrates resilient market appetite for the company’s offerings.

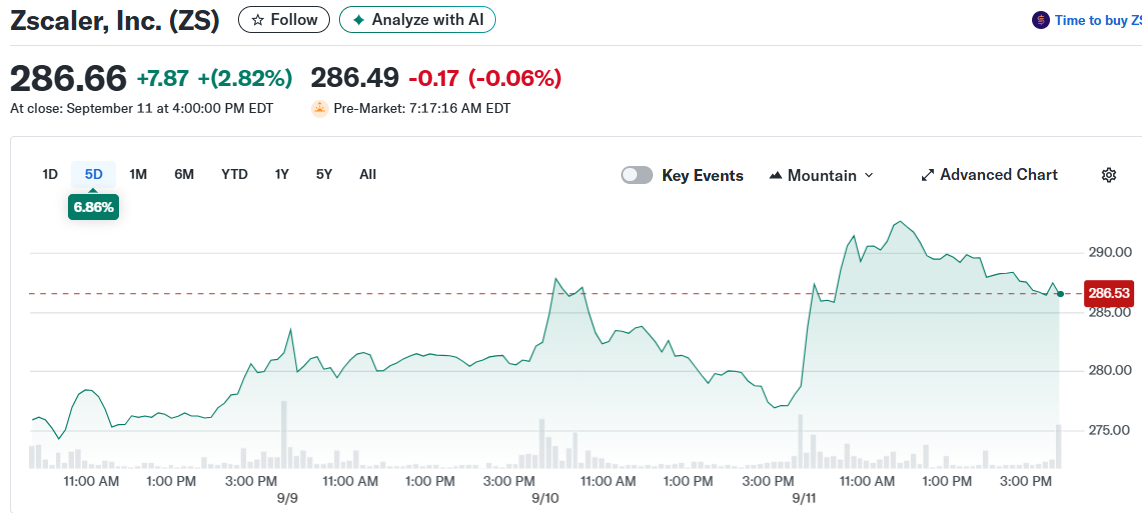

Initial investor reaction to quarterly results was mixed due to a surprise net loss. However, shares have generally trended upward since the post-earnings selloff, with Thursday’s nearly 3% gain outpacing the S&P 500’s 0.8% advance.

Valuation Remains Attractive Despite Rally

Zscaler trades at 16 times sales, below Nvidia’s 25 times sales ratio. While this exceeds the technology sector average of 8.5 times sales, analysts expect Zscaler’s growth to potentially surpass Nvidia’s in coming years.

Wall Street projects continued double-digit revenue expansion for Zscaler over the next three fiscal years. Consensus estimates have been rising recently, reflecting improving company fundamentals and market positioning.

Nvidia’s massive revenue base makes sustaining high growth rates increasingly challenging. Zscaler’s smaller scale and exposure to fast-growing AI cybersecurity segments could support stronger long-term expansion rates.

The cybersecurity company’s stock closed Thursday at $286.66, representing a market capitalization of $45 billion. Current trading levels remain well positioned for further upside based on analyst price targets.

Get 3 Free Stock Ebooks

Discover top-performing stocks in AI, Crypto, and Technology with expert analysis.

- Top 10 AI Stocks - Leading AI companies

- Top 10 Crypto Stocks - Blockchain leaders

- Top 10 Tech Stocks - Tech giants