TLDR

- Alibaba Cloud opened its second Dubai data centre as part of a $53 billion three-year investment in cloud infrastructure.

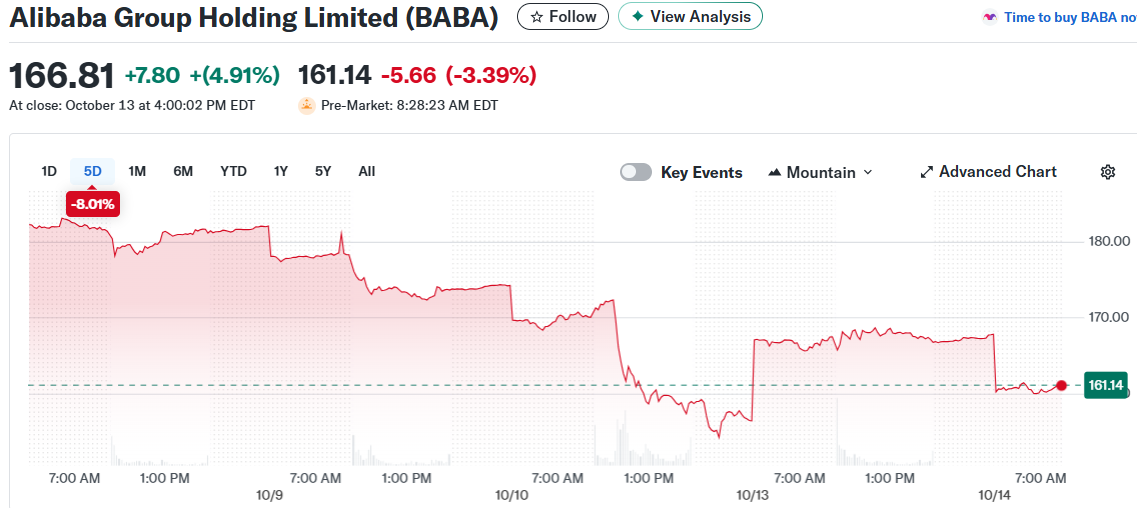

- BABA stock has jumped 100% year-to-date, powered by strong cloud revenue growth of 26% year-over-year.

- Q1 fiscal 2026 revenue reached $34.6 billion with cloud sales hitting 33.4 billion yuan.

- Analysts maintain Strong Buy ratings with 19 Buy and 2 Hold recommendations, projecting 17.69% upside to $196.32.

- The Middle East expansion includes partnerships with regional companies like Abu Dhabi’s Wio Bank during GITEX Global.

Alibaba Cloud launched its second data centre in Dubai on Tuesday. The facility represents the company’s continued investment in Middle Eastern cloud infrastructure.

The expansion arrives nine years after Alibaba’s first Dubai operation. It’s part of a 380 billion yuan commitment over three years.

Eric Wan, vice president of Alibaba Cloud International, pointed to the region’s AI adoption speed. The Middle East offers opportunities for companies looking to deploy artificial intelligence solutions quickly.

The UAE has been pouring billions into AI development. The country is constructing the largest AI campus outside America through deals with Nvidia and OpenAI.

Alibaba Cloud formed partnerships with multiple companies during the GITEX Global exhibition in Dubai. Wio Bank, backed by Abu Dhabi, joined as a partner to leverage local infrastructure for AI deployment.

Stock Surges Over 100% This Year

BABA shares have doubled year-to-date. The rally reflects strong performance in retail operations and cloud services.

TipRanks‘ AI Analyst assigned Alibaba a 75 out of 100 score with an Outperform rating. The analysis suggests a $179 price target, indicating 7.3% upside.

First quarter fiscal 2026 results showed revenue of 247.7 billion yuan or $34.6 billion. Cloud revenue increased 26% year-over-year to 33.4 billion yuan.

The SAP partnership expands Alibaba’s enterprise cloud capabilities. The collaboration brings additional business tools to the platform.

Challenges Remain Despite Growth

Lower adjusted EBITDA presents profitability concerns. New project investments continue generating cash outflows.

The quick commerce division reported losses. Food delivery and fast-service competition remains fierce across markets.

Wall Street keeps a bullish stance despite these headwinds. Nineteen analysts rate the stock as Buy while two recommend Hold.

The average price target stands at $196.32. This implies 17.69% potential upside from current levels.

The Dubai data centre adds capacity for regional cloud and AI services. Revenue growth in cloud computing continues supporting the stock’s strong performance this year.

Get 3 Free Stock Ebooks

Discover top-performing stocks in AI, Crypto, and Technology with expert analysis.

- Top 10 AI Stocks - Leading AI companies

- Top 10 Crypto Stocks - Blockchain leaders

- Top 10 Tech Stocks - Tech giants