TLDR

- David Solomon, CEO of Goldman Sachs, projects oil prices may hit $80–$100 per barrel over the next three to six months

- A severe escalation in the Iran conflict could drive crude prices to $170 per barrel, Solomon cautioned

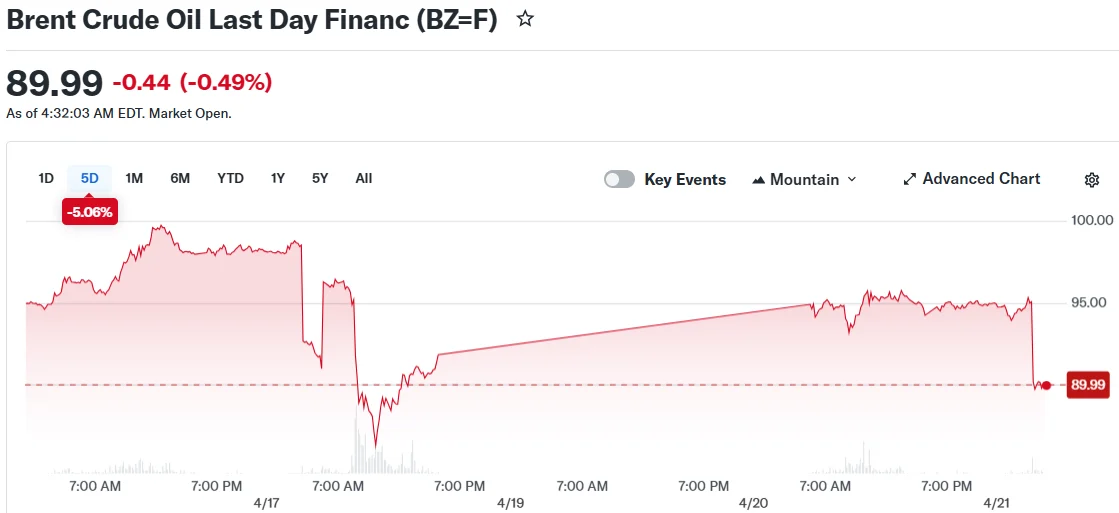

- Brent crude declined 0.5% to $94.95 while WTI slipped 1.8% to $88.04 during Tuesday’s session

- The Strait of Hormuz has remained predominantly closed since hostilities commenced in late February

- Middle Eastern producers Saudi Arabia and UAE have increased alternative route shipments to 6.5 million barrels daily

David Solomon, the chief executive of Goldman Sachs, indicated Tuesday that crude oil prices are likely to climb to a range of $80 to $100 per barrel over the coming three to six months. His remarks came during an appearance at the Paley Center.

Solomon further cautioned that a significant escalation in hostilities involving Iran could send oil prices soaring to $170 per barrel. While he noted that current U.S. recession risks remain relatively modest, he emphasized the volatility of the situation, suggesting conditions could shift dramatically with just “one tweet.”

Oil prices retreated on Tuesday as traders digested conflicting reports regarding diplomatic negotiations between the U.S. and Iran. A temporary cessation of hostilities is scheduled to conclude later this week, though officials have not disclosed the precise expiration date.

Brent crude futures decreased 0.5% to settle at $94.95 per barrel. U.S. West Texas Intermediate declined 1.8% to close at $88.04 per barrel.

The previous trading session had witnessed sharp gains following a weekend escalation in regional tensions. U.S. forces confiscated an Iranian-flagged vessel, prompting Tehran to issue retaliatory warnings.

Iran subsequently closed the Strait of Hormuz once more, reversing its Friday decision to reopen the critical waterway. Iranian authorities justified the move by citing continued U.S. naval blockades along Iranian coastal areas and ports.

Diplomatic Progress Uncertain

President Trump stated Monday that American naval forces would maintain their blockade positions until a comprehensive peace agreement is finalized. He also indicated that fresh diplomatic discussions with Iran were anticipated this week, with U.S. representatives scheduled to travel to Pakistan on Tuesday or Wednesday.

However, Iranian leadership has publicly rejected additional negotiation rounds. Mohammad Bagher Ghalibaf, Iran’s Parliamentary Speaker and chief negotiator, declared that Iran would refuse to engage in talks “under the shadow of threats” from the United States.

Multiple Iranian state-controlled media outlets echoed this stance. Nevertheless, alternative reports suggest Iran has privately informed regional intermediaries of its willingness to dispatch a delegation to Pakistan this week.

Analysts at ANZ wrote that “ongoing uncertainty continues to overshadow any peace agreement, as Iran remains reluctant to attend a second round of talks in Pakistan.”

The two-week ceasefire was formally announced by Trump on April 7 at 6:32 p.m. ET.

Strategic Strait Remains Disrupted

The Strait of Hormuz serves as a transit point for approximately 20% of global oil supplies. The waterway has been substantially closed since armed conflict erupted in late February.

While the initial price surge has moderated somewhat, crude oil values remain considerably elevated compared to pre-conflict levels.

Saudi Arabia and the United Arab Emirates have adapted by redirecting their oil shipments through alternative routes, bypassing the Hormuz chokepoint. These shipments now flow through the Yanbu export terminal on the Red Sea and the Fujairah facility on the Gulf of Oman.

According to ANZ research, total loading volumes at these two alternative terminals have climbed to 6.5 million barrels per day, representing a significant increase from the pre-war level of 5.0 million barrels per day.

The Iran ceasefire deadline approaches with no confirmed diplomatic breakthrough in sight.

Get 3 Free Stock Ebooks

Discover top-performing stocks in AI, Crypto, and Technology with expert analysis.

- Top 10 AI Stocks - Leading AI companies

- Top 10 Crypto Stocks - Blockchain leaders

- Top 10 Tech Stocks - Tech giants