Key Takeaways

- Banking deposits could decline by 3%–5% within five years due to stablecoin adoption, according to Jefferies analysis

- Industry-wide earnings may contract by approximately 3% as lenders turn to costlier funding sources

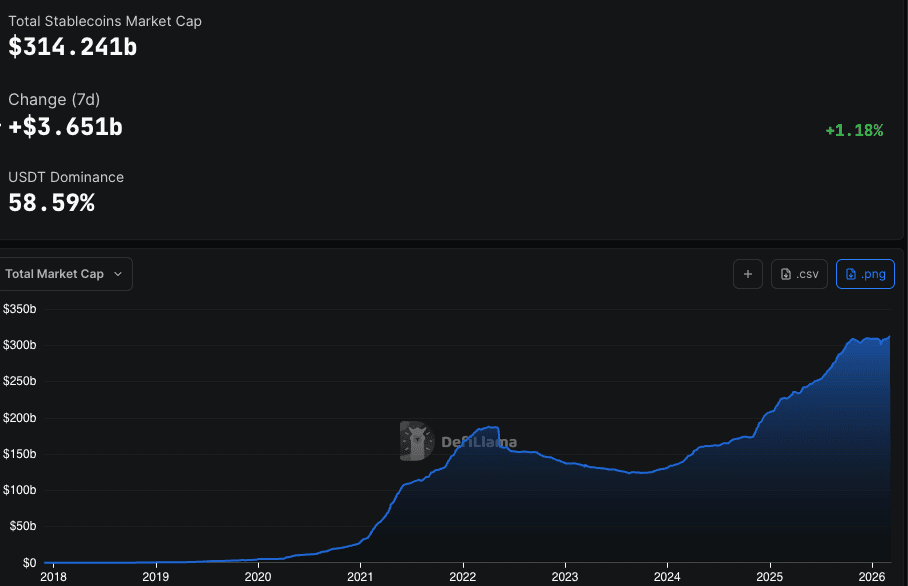

- Stablecoin market capitalization reached $314 billion with projections targeting $1.15 trillion by 2031

- Federal GENIUS Act legislation prevents stablecoin platforms from offering yields to passive users, slowing immediate disruption

- Regional institutions including Wintrust Financial and Webster Financial identified as most vulnerable

The stablecoin industry continues its rapid expansion. Current market valuation stands at approximately $314 billion, representing substantial growth from the $184 billion recorded in 2022.

A recent analysis from Jefferies suggests this expansion poses a meaningful threat to conventional banking profitability over the medium term. The investment bank’s research indicates financial institutions may experience a 3% to 5% erosion of their core deposit base during the coming five-year period.

This migration of deposits would force banks toward more costly funding alternatives. Research team led by David Chiaverini projects average earnings across the sector could contract by approximately 3%.

“The intermediate-term risk of gradual deposit runoff from emerging activity-based yield opportunities and payments use cases should not be ignored,” the analysts wrote.

Stablecoins represent digital currencies anchored to traditional fiat money such as the U.S. dollar. These instruments have gained traction in cryptocurrency markets and are increasingly penetrating payments infrastructure, corporate treasury operations, and international money transfers.

Transaction volume for stablecoins climbed to $11.6 trillion throughout 2025. Outstanding supply reached $305 billion by year-end 2025, marking a 49% year-over-year increase.

Jefferies forecasts the total addressable market for stablecoins could expand to between $800 billion and $1.15 trillion over the next five years.

Banking Executives Sound the Alarm

Bank of America CEO Brian Moynihan warned earlier this year that the banking system could be hurt by the “possibility of $6 trillion in deposits” moving into stablecoins and stablecoin-linked products.

Digital currencies operate continuously without traditional banking hours and integrate seamlessly with decentralized financial protocols offering returns that often exceed conventional savings products. These characteristics create compelling value propositions for consumers seeking enhanced returns on idle capital.

However, recent U.S. regulatory developments have mitigated some immediate threats. The GENIUS Act, which became law in July 2025, prohibits regulated stablecoin operators from distributing yields to passive token holders.

This regulatory framework constrains the velocity at which consumer deposits might migrate from traditional checking and savings products into stablecoin alternatives.

Financial Institutions Launch Competitive Responses

Several prominent financial services companies are proactively entering the space. Fidelity Investments has already introduced its proprietary stablecoin offering, branded as the Fidelity Digital Dollar.

Bank of America’s Moynihan indicated the institution stands ready to launch a stablecoin should Congressional authorization materialize. Goldman Sachs leadership revealed significant internal resources dedicated to tokenization initiatives and stablecoin development.

Jefferies’ analysis indicates that banks maintaining higher concentrations of retail customer deposits and interest-bearing account products face disproportionate vulnerability compared to larger money-center institutions already building digital asset capabilities.

The research specifically identifies Wintrust Financial, Flagstar Financial, Webster Financial, Eagle Bancorp, and Axos Financial as the institutions facing greatest exposure among those covered in the analysis.

The Jefferies report was published on Tuesday, March 10, 2026.

Get 3 Free Stock Ebooks

Discover top-performing stocks in AI, Crypto, and Technology with expert analysis.

- Top 10 AI Stocks - Leading AI companies

- Top 10 Crypto Stocks - Blockchain leaders

- Top 10 Tech Stocks - Tech giants