Key Highlights

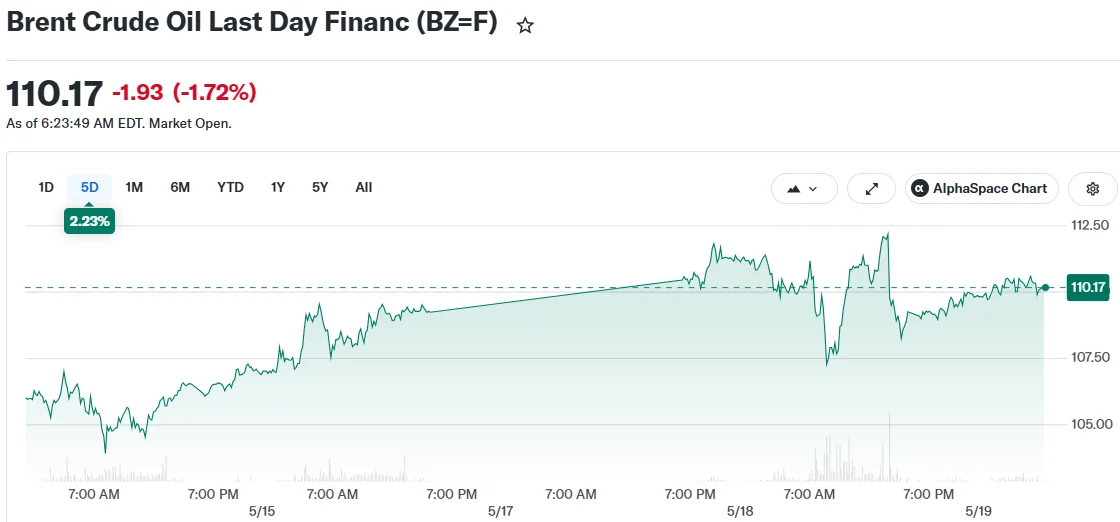

- Brent crude declined 1.5% to settle at $110.39 following Trump’s announcement of a postponed Iranian strike

- Gulf leaders from Saudi Arabia, Qatar, and UAE urged Washington to delay action citing active diplomatic channels

- Year-to-date crude benchmarks have surged more than 80%, with a 20% jump in the last 30 days alone

- Iran’s Kharg Island export hub remains inactive for a minimum of 10 days under US naval blockade

- Washington rolled over its sanctions exemption for seaborne Russian crude for an additional month

Crude oil markets experienced a pullback Tuesday following President Donald Trump’s disclosure that he had suspended planned military operations against Iran after receiving diplomatic appeals from regional Gulf partners.

Brent crude futures retreated 1.5% to $110.39 per barrel, while West Texas Intermediate decreased 0.7% to $103.64. Despite the decline, both major benchmarks continue trading substantially higher than their January levels.

Gulf Nations Intervene as Trump Postpones Military Action

In a social media statement, Trump revealed that leadership from Saudi Arabia, Qatar, and the United Arab Emirates requested the United States postpone strikes scheduled for Tuesday. The president indicated that “serious negotiations” with Tehran were currently in progress.

“I put it off for a little while, hopefully maybe forever, but possibly for a little while,” Trump remarked during a Monday evening White House appearance.

The president cautioned that military options remained on the table should diplomatic efforts fail to produce an acceptable agreement, though no specific timeline was provided.

Market participants seem to have already factored in much of this geopolitical uncertainty. Industry observers note that Trump’s public statements are generating diminished market reactions compared to earlier instances.

“These hot air verbal interventions from Trump used to have a heavy bearish impact on prices, but they now seem to have less and less effect unless they are backed by reality,” said Bjarne Schieldrop, chief commodities analyst at SEB AB.

Tehran has not publicly acknowledged any renewed diplomatic engagement.

Hormuz Strait Blockade Sustains Elevated Crude Valuations

The Strait of Hormuz continues to command market attention as a critical passage for Persian Gulf petroleum shipments, with its effective shutdown maintaining pressure on worldwide supplies.

United States naval forces have enforced a blockade leaving Iran’s primary Kharg Island export facility dormant for no less than 10 days. This action has eliminated Tehran’s oil revenue stream while removing millions of barrels from global circulation.

In the conflict’s initial phase, Iran had prohibited other countries’ tanker traffic through the strait, positioning itself as the sole crude exporter utilizing the passage. Current circumstances have completely reversed this dynamic.

Market specialists suggest substantial price declines are improbable without concrete progress toward reopening the strategic waterway.

Oil benchmarks have climbed over 80% year-to-date and advanced 20% within the previous month, underscoring the severity of supply chain disruptions caused by the ongoing crisis.

Russian Crude Sanctions Relief Prolonged

In a separate development, Washington extended its sanctions exemption covering Russian crude petroleum already aboard tankers for an additional 30-day period.

Treasury Secretary Scott Bessent explained the extension would contribute to physical crude market stabilization while ensuring petroleum deliveries to nations facing the greatest “energy-vulnerability.”

The prior waiver had expired mere days before the renewed authorization took effect.

As of Tuesday’s close, crude prices maintain elevated levels with no definitive resolution emerging regarding the Strait of Hormuz situation.

Get 3 Free Stock Ebooks

Discover top-performing stocks in AI, Crypto, and Technology with expert analysis.

- Top 10 AI Stocks - Leading AI companies

- Top 10 Crypto Stocks - Blockchain leaders

- Top 10 Tech Stocks - Tech giants