Eyes Massive $14B U.S. Market Debut Amid AI Boom")

Key Takeaways

- SK Hynix is preparing to launch American depositary receipts (ADRs) in U.S. markets, potentially raising as much as $14 billion during the latter half of 2026.

- First-quarter 2026 results showed unprecedented operating profit reaching 45 trillion won, accompanied by an exceptional 72% operating margin.

- Shares have skyrocketed approximately 158% year-to-date, driving the company’s valuation near $948 billion.

- Second-quarter HBM revenue projections stand at $7.5 billion, marking an 81% increase compared to January export figures.

- Key challenges include ongoing subcontractor labor tensions, foreign exchange fluctuations, and the threat of U.S. import tariffs on semiconductors.

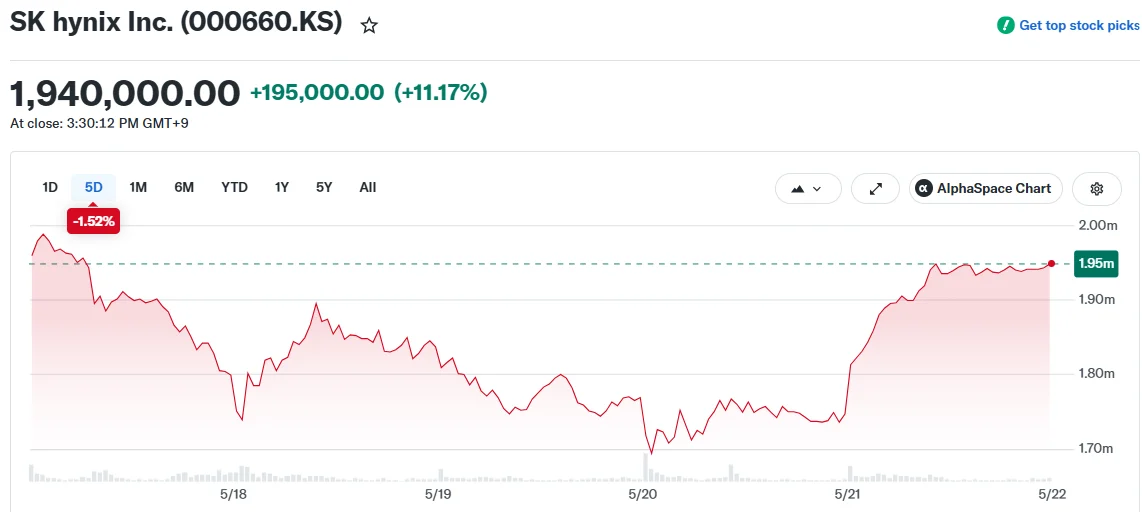

SK Hynix shares experienced a dramatic 11% surge during Wednesday’s Korean trading session as anticipation builds around the chipmaker’s forthcoming American market debut.

The memory semiconductor specialist from South Korea is moving forward with plans to introduce American depositary receipts (ADRs) on U.S. exchanges, with industry sources indicating a potential launch window between June and July. According to reports from Korean financial media, the offering could generate proceeds reaching $14 billion, earmarked for financing manufacturing facilities in both South Korea and Indiana.

This strategic move would provide American portfolio managers with direct exposure to a leading AI memory manufacturer outside of Micron Technology. Previously, Micron has served as the dominant avenue for U.S.-based investors seeking participation in the high-bandwidth memory (HBM) sector.

Currently, SK Hynix commands a forward price-to-earnings multiple of approximately 6.1x, notably lower than Micron’s 8.3x valuation. This pricing disparity has attracted considerable interest from investors hunting for undervalued opportunities within the artificial intelligence chip ecosystem.

The company’s market capitalization currently hovers around $948 billion, positioning it tantalizingly close to joining the exclusive trillion-dollar club. Share prices have nearly tripled throughout 2026.

Blockbuster Financial Performance Fuels Momentum

First-quarter 2026 revenue registered at 52.5763 trillion won, delivering a remarkable 72% operating margin — metrics that underscore the persistent imbalance between constrained HBM supply and surging market demand.

Analysts at Bernstein project SK Hynix will deliver approximately $7.5 billion in HBM-related revenue during Q2 2026, representing a 25% quarter-over-quarter increase. While this estimate falls short of a previous $8.2 billion projection, export statistics from North Chungcheong and Icheon facilities revealed an impressive 81% spike from January baselines.

Extended supply agreements are providing a protective buffer for HBM pricing stability, insulating the segment from the cyclical swings that typically plague traditional memory chip markets.

During Dell Technologies World 2026, SK Hynix unveiled its HBM4 and HBM3E offerings alongside enterprise server memory solutions and solid-state drives designed for AI-enabled PCs, demonstrating its strategic expansion beyond traditional data center applications into consumer-facing products.

Workforce Tensions and Competitive Dynamics

However, the path forward isn’t entirely friction-free. A labor organization representing employees at P&S Logis, a logistics subcontractor, is preparing litigation over significant compensation disparities between SK Hynix’s direct workforce and subcontracted personnel.

The union intends to leverage the “Yellow Envelope Act,” legislation effective since March that empowers subcontracted workers to engage in direct wage negotiations with principal companies.

Meanwhile, a potentially advantageous development is unfolding at competitor Samsung Electronics, where an 18-day work stoppage is scheduled to commence Thursday. Any production interruptions at Samsung facilities could redirect customer procurement toward SK Hynix.

SK Hynix already surpassed Samsung to become South Korea’s most valuable non-financial corporation by market capitalization earlier this year, powered predominantly by its commanding position in HBM technology.

Regarding product development, initial HBM4E engineering samples are slated for delivery in the second half of 2026, with volume manufacturing targeted for 2027.

Specific details regarding the ADR offering size and share pricing remain unconfirmed. Prospective investors should weigh currency volatility and the possibility of U.S. tariffs on semiconductor imports when evaluating the upcoming American market listing.

Get 3 Free Stock Ebooks

Discover top-performing stocks in AI, Crypto, and Technology with expert analysis.

- Top 10 AI Stocks - Leading AI companies

- Top 10 Crypto Stocks - Blockchain leaders

- Top 10 Tech Stocks - Tech giants