Key Takeaways

- Since late February’s geopolitical escalation, Treasury yields have climbed dramatically, with the 30-year bond reaching levels not seen in nearly two decades.

- April’s consumer price index registered 3.8%, with analysts projecting a potential surge to 6.7% by the second quarter as energy costs ripple through the economy.

- Market expectations have shifted dramatically: the Federal Reserve is now anticipated to raise rates by early 2027, completely reversing earlier projections of two cuts this year.

- Historical data reveals a consistent pattern: the S&P 500 has declined following each Fed rate-hike cycle launch since 1999, averaging a 7% pullback.

- Equity markets rallied on diplomatic breakthrough optimism, yet bond traders remained skeptical as they await critical economic data releases scheduled for Thursday.

Geopolitical conflict has triggered an inflation spike, propelled Treasury yields to levels unseen in years, and fundamentally altered Federal Reserve policy expectations from accommodation to tightening. Here’s an analysis of these developments and their implications for market participants.

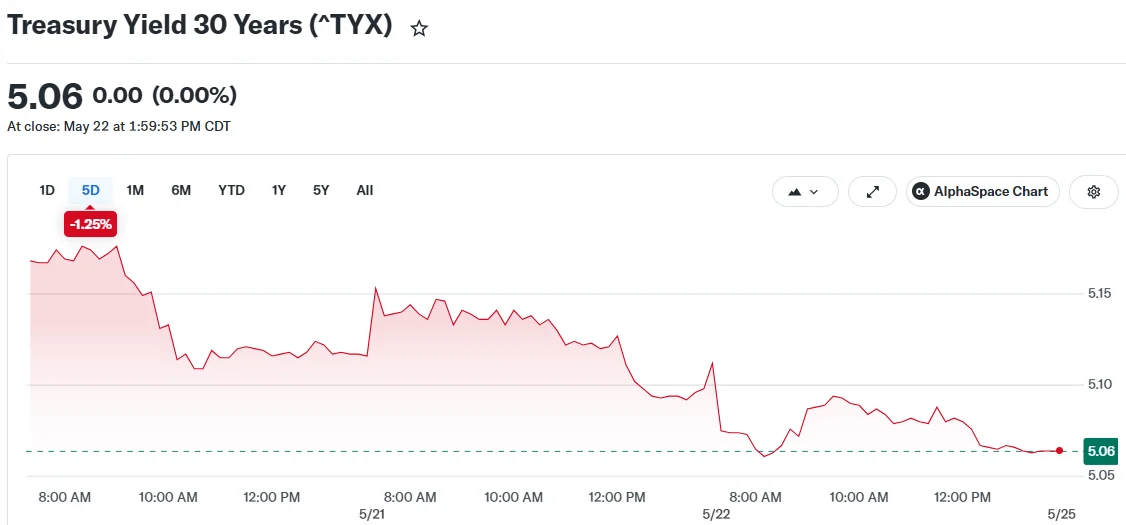

Bond Yields Reach Multi-Decade Highs

Following the outbreak of hostilities in late February, oil prices skyrocketed after Iran’s closure of the Strait of Hormuz disrupted a critical artery for global petroleum transport. This energy shock reverberated throughout the economic system, driving up costs across multiple sectors.

April’s consumer price inflation registered at 3.8%, marking the most elevated reading since 2023. Forecasters at the Federal Reserve Bank of Cleveland anticipate this figure could climb as high as 6.7% during the second quarter.

As inflationary pressures intensified, bond investors began liquidating Treasury holdings en masse. This selling pressure drove bond prices downward, which inversely pushed yields upward. The 2-year Treasury yield has climbed 75 basis points since hostilities commenced. Meanwhile, the 30-year bond now offers returns exceeding 5%, representing the highest yield in 19 years.

At the year’s outset, market participants widely anticipated at least two Federal Reserve rate reductions. However, according to CME Group’s FedWatch tool, expectations have completely reversed, with the next anticipated policy move being a rate increase potentially arriving as soon as January 2027.

Historical Precedent Shows Equity Vulnerability During Rate-Hike Cycles

Elevated interest rates increase capital costs for corporations, potentially dampening investment activity and compressing profit margins. Additionally, higher rates create headwinds for consumer purchases of major items requiring financing.

Looking back to 1999, the Federal Reserve has initiated four distinct rate-hike cycles. The S&P 500 experienced losses following every single cycle initiation within the subsequent three-month period. The mean decline measured 7%, with individual episodes ranging from 1% to 17% drawdowns.

The S&P 500 currently shows approximately 9% year-to-date gains, buoyed by robust corporate earnings results. However, some market strategists caution that the rally may be obscuring underlying vulnerabilities.

“The S&P 500 is still riding a wave of euphoria from a blowout earnings season, but with that over for the next couple of months, the likelihood of a summer selloff is high,” said Dennis Follmer, chief investment officer at Montis Financial.

Diplomatic Progress Boosts Equities While Bond Traders Remain Cautious

Tuesday witnessed a significant equity market rally following reports suggesting imminent completion of diplomatic negotiations. The Nasdaq surged approximately 300 points, propelled by gains in technology giants including Nvidia, Intel, and Micron Technology. The S&P 500 opened nearly 50 points higher.

Energy markets experienced notable volatility. Brent crude jumped more than 3% to reach $96.43 per barrel during early trading hours, although prices remain approximately 8.6% below Friday’s closing level.

Secretary of State Marco Rubio indicated negotiations had reached final stages but cautioned that completion might require “a few more days.” Simultaneously, Iran’s Revolutionary Guard alleged it had engaged a U.S. aircraft that violated Iranian airspace, introducing uncertainty regarding the diplomatic timeline.

Fixed-income markets displayed considerably less enthusiasm. The 10-year Treasury yield maintained levels above 4.5%. The 30-year remained firmly above 5%. Market participants are maintaining a defensive posture ahead of Thursday’s release of April inflation metrics and first-quarter gross domestic product figures.

“Bond markets are sending a pretty strong signal that they see choppier waters ahead,” Follmer added.

Paul Donovan, global chief economist at UBS Wealth Management, acknowledged progress in talks but said “a deal still seems some way off.”

This week’s economic calendar includes new residential sales data and weekly unemployment claims filings, alongside Thursday’s inflation and GDP releases. These indicators will likely determine market sentiment heading into the week’s conclusion.

Get 3 Free Stock Ebooks

Discover top-performing stocks in AI, Crypto, and Technology with expert analysis.

- Top 10 AI Stocks - Leading AI companies

- Top 10 Crypto Stocks - Blockchain leaders

- Top 10 Tech Stocks - Tech giants