Earnings, Treasury Yields, and Major Retail Reports Ahead")

Quick Overview

- Nvidia’s first-quarter report arrives Wednesday with Wall Street forecasting $1.78 earnings per share and $79.2 billion revenue

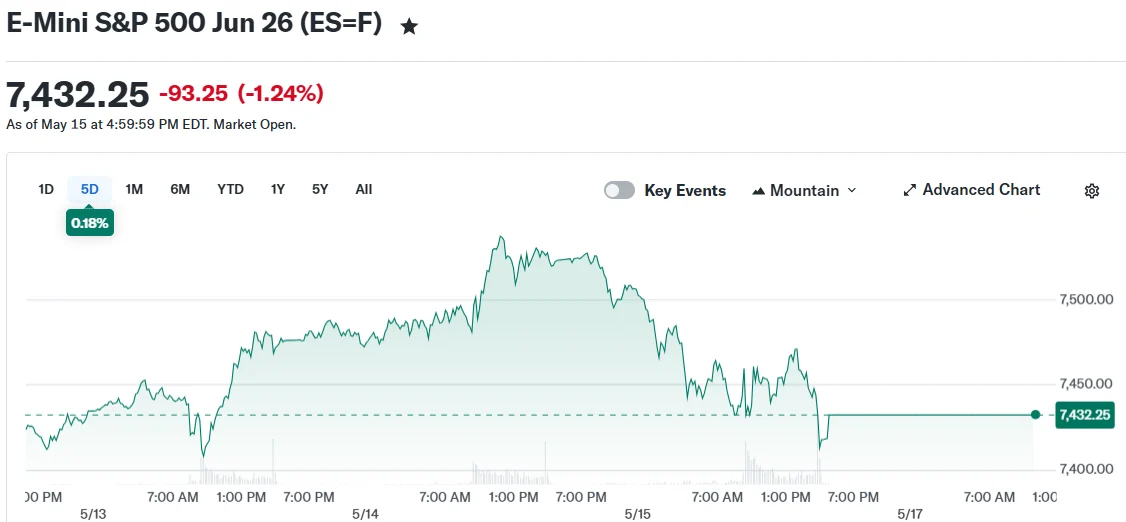

- Major indexes stumbled Friday with the S&P 500 declining 1.2%, snapping a seven-week winning momentum

- Treasury yields crossed the 4.5% threshold on the 10-year note, intensifying market headwinds

- Carlyle Group’s Jeff Currie forecasts commodities may be launching into an extended multi-year rally

- Walmart’s Thursday earnings will test consumer strength as April CPI registered 3.8% year-over-year

Market participants enter the coming trading sessions facing multiple headwinds. Friday’s session brought equity declines, bond yield expansion, and lingering uncertainty from recent Trump-Xi diplomatic meetings.

The S&P 500 surrendered 1.2% Friday, though it squeezed out a modest 0.1% advance for the week — marking seven consecutive positive weeks. The Nasdaq tumbled 1.5% in Friday’s session, finishing the week marginally negative at approximately 0.1%. The Dow Jones Industrial Average similarly concluded weekly trading 0.2% lower.

Friday saw the 10-year Treasury benchmark solidly breach 4.5%, a threshold that traditionally triggers concern among equity holders. This metric will remain under close observation as markets open.

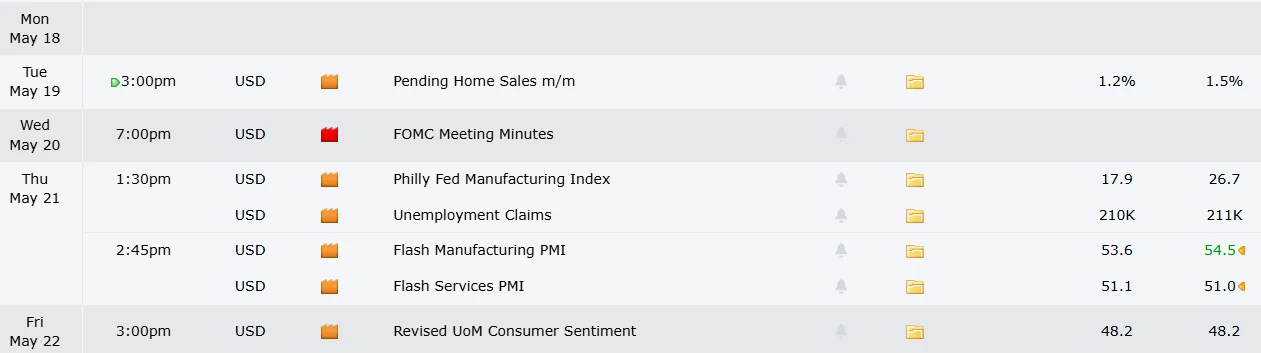

While the economic calendar appears less crowded than previous weeks, one announcement dominates attention.

Nvidia’s Quarterly Report Commands Attention

Nvidia releases its first-quarter financial results Wednesday following the closing bell. The chipmaker currently holds the distinction of being the world’s most valuable corporation, surpassing $5.7 trillion in market capitalization last week.

Wall Street consensus points to adjusted earnings of $1.78 per share with revenue expectations at $79.2 billion.

Back in March, CEO Jensen Huang characterized demand for the company’s products as “off the charts.” He expanded projections for two major product categories, projecting they could generate over $1 trillion combined by late 2026.

Huang recently accompanied President Trump on a China visit, participating in meetings with government officials and corporate executives. Market watchers will scrutinize any remarks regarding potential agreements or transactions from that diplomatic mission.

Reports surfaced last week indicating Chinese technology giants such as Alibaba, Tencent, ByteDance, and JD.com received authorization to purchase Nvidia’s H200 processors. This development propelled shares to fresh record highs Thursday before Friday’s retreat.

Despite the impressive rally, UBS analyst Tim Arcuri observed subdued enthusiasm among institutional investors approaching the announcement, potentially creating conditions for upside surprise if results exceed expectations.

Bank of America analyst Vivek Arya highlighted that market participants will monitor any discussion regarding competitive pressure from Advanced Micro Devices, Broadcom, and emerging player Cerebrus, which completed its public offering last week.

Walmart, Retail Sector, and Consumer Health

Walmart delivers its quarterly update Thursday morning. Scrutiny will intensify given April’s Consumer Price Index revealed 3.8% annual inflation, primarily fueled by escalating energy prices.

Walmart characterized its customer base as “resilient” last quarter. This week’s report will reveal whether that assessment remains accurate.

Target releases results Wednesday. Newly appointed CEO Michael Fiddelke has articulated strategies to revitalize growth momentum. Home Depot and Lowe’s announce Tuesday and Wednesday respectively, though both face challenges from stagnant housing market conditions.

The University of Michigan’s consumer sentiment index and inflation expectations survey concludes Friday, completing the week’s economic data landscape.

Are Commodities Starting a Multi-Year Bull Market?

Carlyle Group energy strategist Jeff Currie published comprehensive analysis Friday suggesting markets may be witnessing the beginning of an extended commodity upswing.

Currie highlighted AI’s escalating requirements for tangible infrastructure — power generation, industrial metals, and computational resources — as a primary catalyst. He referenced the Iran situation, which Goldman Sachs estimates has eliminated over 13.7 million barrels daily from global markets, representing an unprecedented energy supply disruption.

Currie contends that investment capital has concentrated on the AI trade while the physical commodities essential to AI operations have experienced chronic underinvestment. He projects this disparity is beginning to rebalance.

Get 3 Free Stock Ebooks

Discover top-performing stocks in AI, Crypto, and Technology with expert analysis.

- Top 10 AI Stocks - Leading AI companies

- Top 10 Crypto Stocks - Blockchain leaders

- Top 10 Tech Stocks - Tech giants