Down as Nvidia (NVDA), AMD (AMD), and Micron (MU) Tumble")

Key Takeaways

- Semiconductor stocks experienced their second consecutive day of heavy losses, pulling down U.S. stock futures Tuesday and Wednesday

- Chip giants Nvidia, AMD, and Micron spearheaded the decline, with Micron plummeting 13% in Tuesday’s session

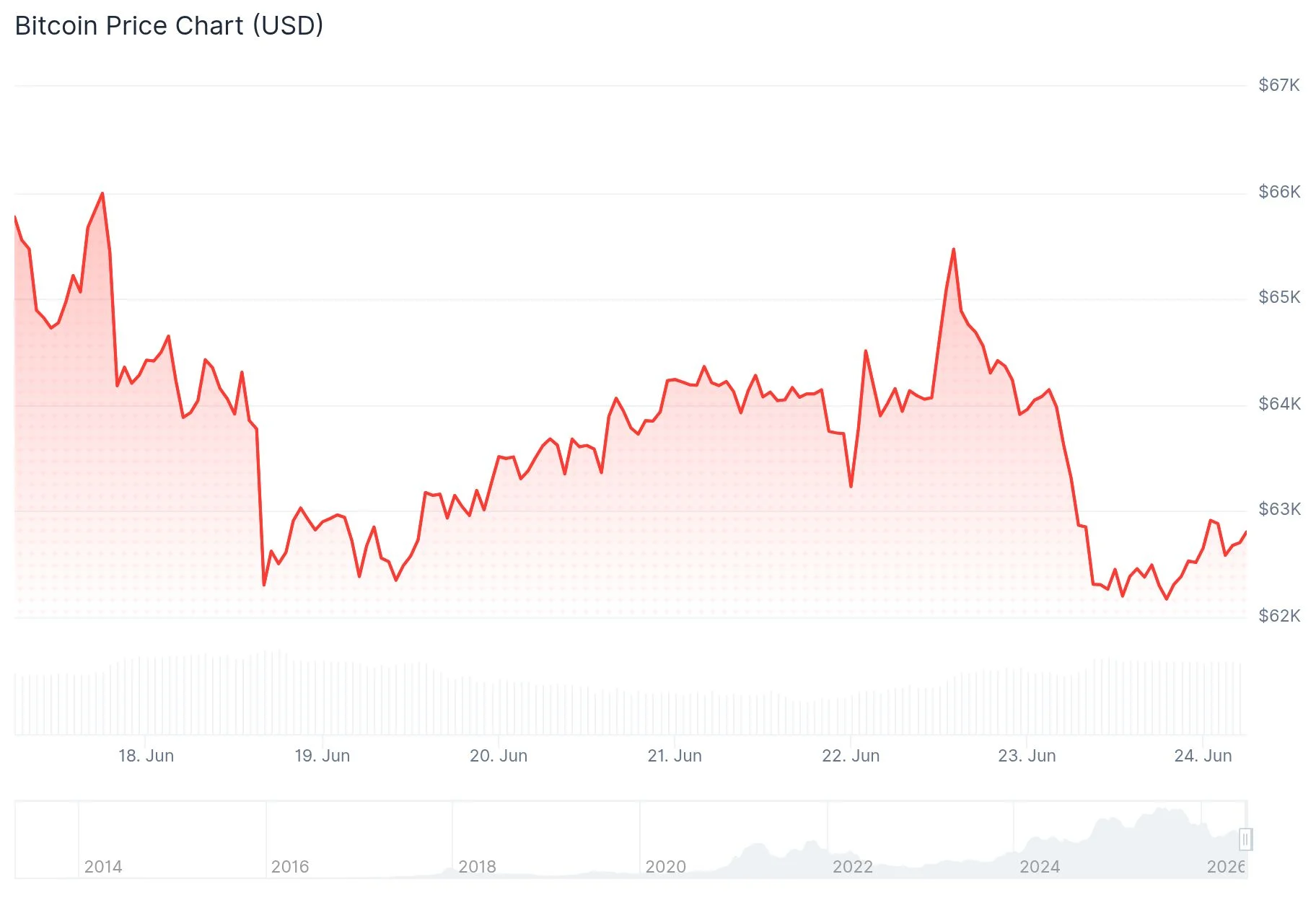

- Bitcoin retreated toward the $62,000 mark, posting a nearly 5% weekly decline, while Ether and XRP suffered steeper losses

- Spot Bitcoin ETFs in the United States posted unprecedented 30-day outflows exceeding $6 billion

- FedEx reported disappointing earnings results, attributing challenges to evolving trade policies

Bitcoin descended toward the $62,000 threshold on Wednesday as the semiconductor sector’s extended selloff entered its second day, pulling down risk-sensitive assets throughout global markets.

Futures contracts for U.S. equities showed weakness, with both Dow and S&P 500 futures declining 0.1%. Nasdaq 100 futures remained relatively unchanged.

The Philadelphia Semiconductor Index suffered a brutal 7.9% decline during Tuesday’s trading session. Every single one of its 30 constituent companies finished in negative territory. Nvidia, Micron, and AMD experienced the most severe drops.

Micron alone shed 13% of its value on Tuesday. The memory chip manufacturer had surged over 250% throughout 2026 before this recent correction. Market participants are anxiously awaiting the company’s quarterly earnings release scheduled for Wednesday evening.

The broader S&P 500 index tumbled 1.4% on Tuesday. The tech-heavy Nasdaq 100 suffered a more pronounced 3.3% decline. A brief recovery attempt in Asian semiconductor stocks on Wednesday morning quickly fizzled, with Taiwan Semiconductor Manufacturing Company sliding more than 3%.

FedEx shares declined following its earnings announcement. The shipping and logistics giant, frequently regarded as a bellwether for overall economic conditions, identified evolving trade policies as a significant obstacle.

Cerebras, a newly public AI chipmaker, released its inaugural earnings report after market close. The stock retreated as market participants questioned whether the company could effectively compete against established semiconductor leaders.

Cryptocurrency Markets Face Intensifying Headwinds

Bitcoin changed hands around $62,546, representing a 2.1% decrease over 24 hours and a 4.9% weekly decline. The flagship cryptocurrency has remained confined to the lower boundary of its monthly trading range.

Ether declined 3.7% to reach $1,661, marking a 7.2% weekly drop. XRP retreated 2.2% to $1.10, registering a 9.3% decline across the week. Solana decreased 3.3% to $69. Dogecoin experienced a 9.8% seven-day slide.

Hyperliquid’s HYPE token suffered the most significant damage, plunging 8.8% in a single day and 18.6% over the week to approximately $61. Tron stood as a notable outlier, gaining 3.7% for the week.

Record ETF Withdrawals and Options Expiration Compound Selling Pressure

U.S. spot Bitcoin ETFs documented an unprecedented 30-day net outflow surpassing $6 billion. Mike McCluskey, co-founder of tx, characterized this as persistent institutional risk reduction from the very investors who fueled the current market cycle.

According to McCluskey, until capital flows demonstrate a definitive reversal, any temporary market rebounds will likely encounter significant resistance.

He also highlighted a substantial options expiration event on Deribit scheduled for Friday. Approximately $10.6 billion in notional value is set to expire. Nearly 80% of outstanding positions are currently out of the money, concentrated around a $60,000 put strike and an $80,000 call strike.

The $60,000 price level has already faced testing earlier this month and is widely recognized as a critical technical support zone.

From a macroeconomic perspective, crude oil prices continued their descent. Brent crude decreased roughly 1% toward $76 per barrel. The U.S. dollar climbed to a seven-month peak as market participants gravitated toward traditional safe-haven assets.

Bitcoin finds itself trapped between deteriorating sentiment in AI-related investments and declining oil prices, maintaining support above $60,000 but lacking the momentum for meaningful upside movement while institutional capital remains sidelined.

Get 3 Free Stock Ebooks

Discover top-performing stocks in AI, Crypto, and Technology with expert analysis.

- Top 10 AI Stocks - Leading AI companies

- Top 10 Crypto Stocks - Blockchain leaders

- Top 10 Tech Stocks - Tech giants