Key Highlights

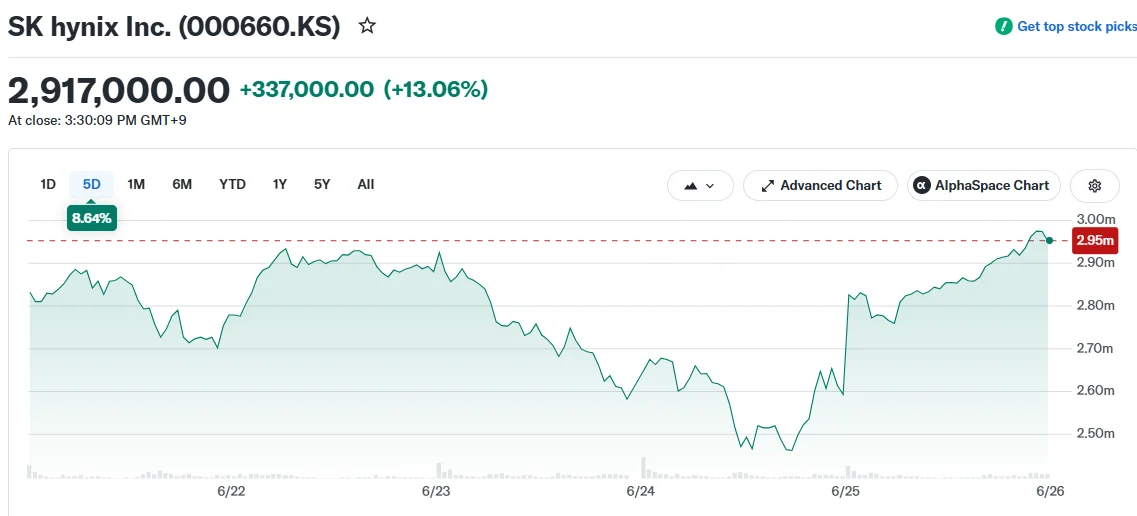

- Shares of SK Hynix climbed 13% during Thursday’s trading session in South Korea

- The memory chipmaker confirmed plans to debut ADRs on Nasdaq July 10, valued at approximately $30 billion

- Micron reported quarterly revenue of $41.5 billion, representing a 346% increase year over year and significantly exceeding analyst projections

- Micron’s leadership anticipates constrained memory supply conditions extending past 2027

- SK Hynix shares have skyrocketed more than 300% throughout 2026, recently surpassing Samsung to claim the title of South Korea’s largest company by market capitalization

Shares of SK Hynix rocketed as high as 15% to an all-time peak of 2,987,000 won during Thursday’s session before settling with gains of approximately 13% in Seoul.

The dramatic rally stemmed from two powerful catalysts converging simultaneously — the chipmaker’s announcement of a landmark American exchange listing and extraordinary quarterly results from competitor Micron.

SK Hynix officially revealed Wednesday its intention to introduce American Depositary Receipts on the Nasdaq Global Select Exchange beginning July 10. The offering is expected to reach a valuation between $29 billion and $30 billion.

Since the disclosure occurred after South Korean exchanges had concluded trading Wednesday, Thursday represented investors’ initial opportunity to respond. The response was emphatic.

The broader KOSPI Index also delivered impressive gains, advancing more than 6%. This marked a continuation of a powerful recovery following a 10% decline witnessed earlier in the week. Year-to-date, the benchmark has surged 112% in 2026.

Micron’s Results Provided Additional Momentum

Micron disclosed quarterly revenue reaching $41.5 billion, substantially surpassing Wall Street’s consensus forecast of $35.9 billion. This figure represents a remarkable 346% jump compared to the prior year.

Forward guidance proved even more impressive. Micron projected approximately $50 billion in revenue for its upcoming fiscal fourth quarter, once again exceeding analyst expectations considerably.

Chief Executive Officer Sanjay Mehrotra indicated the company anticipates constrained market dynamics to continue through 2027 and beyond, fueled by artificial intelligence demand spanning all business segments combined with fundamental supply limitations.

Such forward-looking commentary carries significant implications for SK Hynix. Both corporations compete head-to-head in DRAM and high-bandwidth memory sectors, meaning favorable pricing environments for Micron typically signal similar conditions for SK Hynix.

SK Hynix’s Commanding Memory Market Presence

SK Hynix commands the high-bandwidth memory sector, which has emerged as among the most sought-after components powering AI infrastructure expansion. This strategic position has rendered the stock particularly responsive to artificial intelligence industry developments.

The aggressive buildout of data centers by multinational technology giants has constricted worldwide memory availability throughout the past year. This dynamic has elevated prices for both conventional DRAM and HBM products.

SK Hynix, Micron, and Samsung have each benefited substantially from this demand wave. However, SK Hynix has delivered superior performance compared to both competitors.

The company’s shares have climbed over 300% during 2026 alone, establishing it among the top-performing equities globally throughout the current year.

The stock recently eclipsed Samsung to secure the position of South Korea’s highest-valued enterprise — an achievement that would have appeared improbable until recently.

The forthcoming Nasdaq ADR debut scheduled for July 10 will provide American investors their first opportunity to access the stock directly through an exchange-traded instrument.

Micron’s quarterly financial performance represents the latest confirmation that AI-fueled memory demand continues demonstrating strength as the second half of 2026 approaches.

Get 3 Free Stock Ebooks

Discover top-performing stocks in AI, Crypto, and Technology with expert analysis.

- Top 10 AI Stocks - Leading AI companies

- Top 10 Crypto Stocks - Blockchain leaders

- Top 10 Tech Stocks - Tech giants