Volatility Plunges to 8-Month Minimum as Short Squeeze Looms")

Key Takeaways

- Bitcoin’s implied volatility has declined to 36%, marking an eight-month low

- Concentrated short interest exists in the $78,000-$83,000 price zone

- Bitcoin spot ETFs have witnessed approximately $1.74 billion in net outflows

- Binance’s BTC holdings increased by roughly 16,000 coins over the last month

- Breaking above $82,000 may initiate a cascade of forced short liquidations

Bitcoin’s implied volatility metric has contracted to 36%, representing the most subdued reading in eight months. This indicates that institutional market participants are not anticipating significant directional price action in the near term.

Implied volatility serves as a gauge for expected price fluctuations within derivative markets. When this indicator reaches such compressed levels, it typically signals a market consolidation phase. BTC has remained trapped beneath the $90,000 threshold for approximately four months.

Tyler Evans, who serves as chief investment officer at UTXO Management, identified digital credit mechanisms as a primary factor behind the market’s stability. According to Evans, collateralized lending arrangements have enabled major stakeholders — including mining operations and corporate treasury holders — to maintain their Bitcoin exposure without triggering sales pressure.

Market analyst Daan Crypto Trades offered commentary on X regarding Bitcoin’s current technical position. He noted that BTC appears to be “trying to make a higher low here locally” but emphasized the necessity of clearing the lower $80,000 range to validate the recovery attempt from February’s bottoms. His assessment: no definitive breakout confirmation has materialized yet.

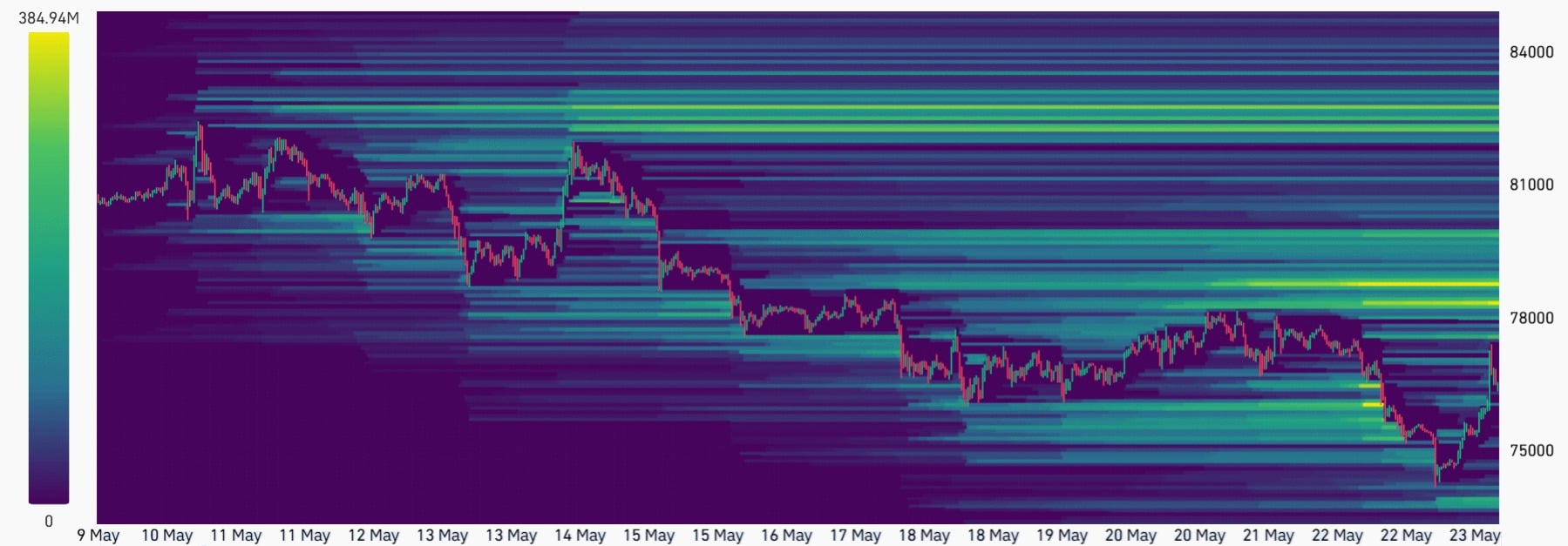

Concentrated Short Interest Creates Squeeze Potential

Liquidation mapping data provided by CoinGlass reveals substantial short position density between $78,000 and $83,000. Bearish traders have apparently gained conviction following months of Bitcoin struggling beneath $90,000.

Put option contracts currently command a 14% premium relative to call options, based on Glassnode’s analytics. During typical market equilibrium, this differential oscillates between -6% and +6%. The current elevated spread has persisted beyond normal ranges for sixteen consecutive weeks.

Should Bitcoin momentum carry prices beyond $82,000, this dense accumulation of bearish positions faces potential forced liquidation, which would trigger automatic buy orders and potentially amplify upward price movement.

Declining Spot Market Interest

From a fundamental demand perspective, indicators paint a less optimistic picture. Spot Bitcoin exchange-traded fund products have registered cumulative outflows exceeding $1.74 billion, while the Coinbase Premium indicator has shifted into deeply negative territory — reflecting diminished institutional buying appetite from U.S. markets.

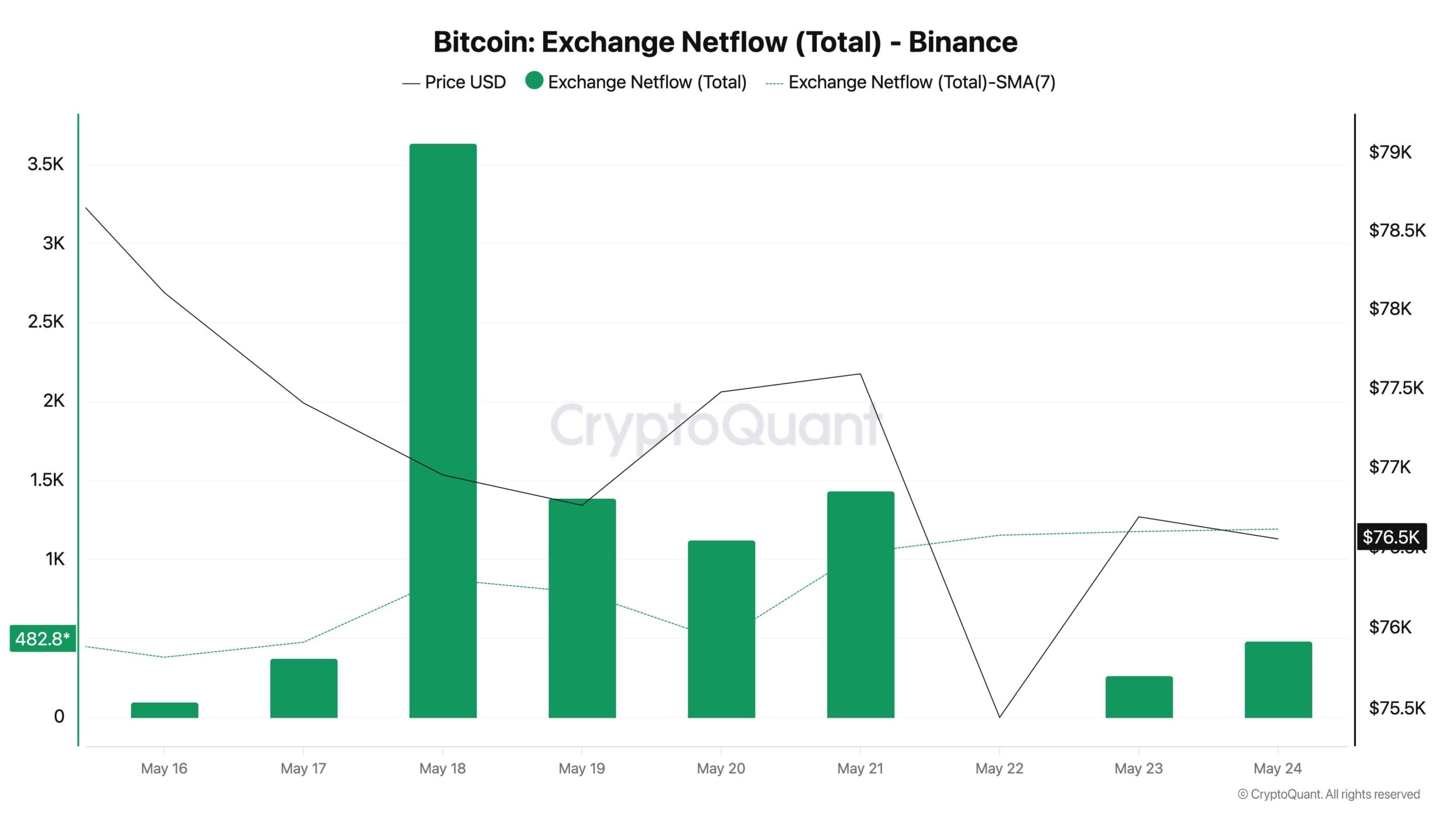

Binance BTC netflows experienced an approximately 425% surge as older wallet holdings migrated back to exchange platforms. Binance daily inflows expanded from roughly 378 BTC on May 16 to nearly 1,190 BTC within a ten-day window, including a notable single-day influx exceeding 3,600 BTC on May 18.

Bitcoin’s Apparent Demand indicator deteriorated to approximately -147,000 BTC, representing the weakest measurement since December 2025. This metric evaluates whether sustained long-term accumulation patterns can adequately offset freshly minted supply entering circulation.

Bitcoin experienced a brief 6.2% price decline coinciding with the period of heightened exchange inflows. Binance’s total BTC reserves expanded from approximately 616,000 BTC to around 632,000 BTC throughout the past thirty days.

Funding rates have maintained positive territory despite these softer demand signals, indicating that leveraged long position holders continue participating actively in derivative markets.

Get 3 Free Stock Ebooks

Discover top-performing stocks in AI, Crypto, and Technology with expert analysis.

- Top 10 AI Stocks - Leading AI companies

- Top 10 Crypto Stocks - Blockchain leaders

- Top 10 Tech Stocks - Tech giants