Key Highlights

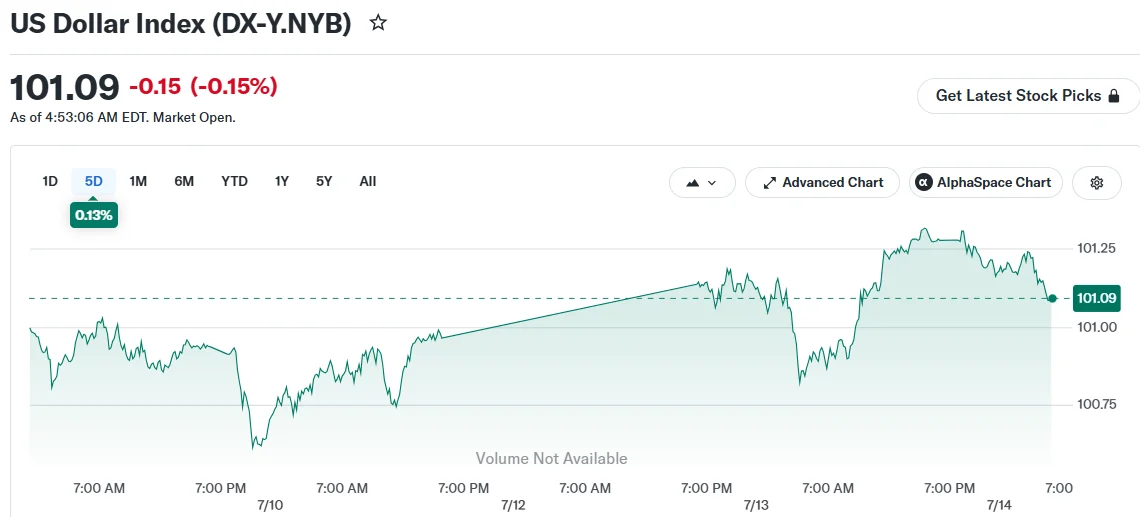

- The Dollar Index maintained support above the 101.00 threshold ahead of critical June CPI releases

- Crude oil price increases fueled by regional geopolitical conflicts are weighing heavily on emerging market currencies including the rupee

- Financial markets indicate approximately 50% probability of Federal Reserve tightening in July

- New Zealand’s currency led gains among major developed market currencies following hawkish Reserve Bank commentary

- The euro faces potential decline toward 1.10 if energy market pressures intensify

The greenback maintained stability on Tuesday as market participants positioned ahead of upcoming inflation figures while crude oil prices extended gains due to intensifying geopolitical tensions across the Middle East. The Dollar Index hovered just above 101.00 throughout European trading sessions.

Consensus estimates for June’s Consumer Price Index point to annual inflation moderating to 3.8%, marking a decline from May’s 4.2% reading. While headline price pressures are projected to ease on a monthly basis thanks to softening energy components, core inflation hovering around 0.2% month-over-month remains insufficient to alleviate concerns regarding stubborn underlying price dynamics.

Federal Reserve Tightening Expectations Climb

Current market pricing reflects approximately 50% odds of the Federal Reserve implementing a rate increase during July’s policy meeting, with cumulative tightening of roughly 43 basis points anticipated through year-end. Fed Governor Chris Waller indicated Monday that additional monetary tightening might prove necessary in the near term should core inflation metrics remain persistently elevated.

Chair Kevin Warsh commenced his inaugural House testimony on Tuesday. Additional Fed officials including Barr, Goolsbee, Cook and Bowman were slated to deliver remarks throughout the trading day.

Analysts at ING suggest the Dollar Index could rapidly advance to 102.0 should the Strait of Hormuz blockade situation persist.

Energy Markets and Regional Tensions Shape FX Landscape

Brent crude advanced to $84 per barrel on Tuesday, buoyed by continued US military operations marking the third straight day of strikes on Monday. Iranian media outlets documented explosions occurring near Kish, Qeshm, Abu Musa and the coastal hub of Bandar Abbas.

US petroleum stockpiles, encompassing both commercial and strategic petroleum reserves, registered 730.8 million barrels as of July 3, representing the most constrained supply level observed since 1984.

The Indian rupee declined to a fresh seven-week trough versus the dollar, with the exchange rate approaching 96.13. Domestic crude futures contracts opened with gains exceeding 4% during the trading session.

The euro retreated beneath the 1.1400 threshold against the greenback. EUR/USD faces potential downside momentum toward 1.10 should Brent crude escalate to the $90-$100 per barrel range while European natural gas prices advance to €55-€60 per megawatt hour.

European Central Bank President Christine Lagarde was scheduled to convene with US Treasury Secretary Scott Bessent on Tuesday and present remarks addressing the economic landscape.

The New Zealand dollar emerged as the strongest performer among G10 currencies this week. The kiwi appreciated approximately 0.8% on Tuesday following Reserve Bank of New Zealand Chief Economist Paul Conway’s comments suggesting additional monetary policy tightening may be warranted should Middle East-related inflation pressures demonstrate persistence. Markets currently price in 60 basis points of policy tightening in New Zealand through year-end.

The Japanese yen traded in a narrow range above the 162.00 mark. Japan’s Finance Minister Satsuki Katayama noted that significant shifts in the asset management landscape could trigger a reassessment of the Government Pension Investment Fund’s allocation strategy.

The British pound stabilized near 1.3350 as traders awaited UK GDP figures for May, scheduled for release later this week.

Get 3 Free Stock Ebooks

Discover top-performing stocks in AI, Crypto, and Technology with expert analysis.

- Top 10 AI Stocks - Leading AI companies

- Top 10 Crypto Stocks - Blockchain leaders

- Top 10 Tech Stocks - Tech giants