Key Takeaways

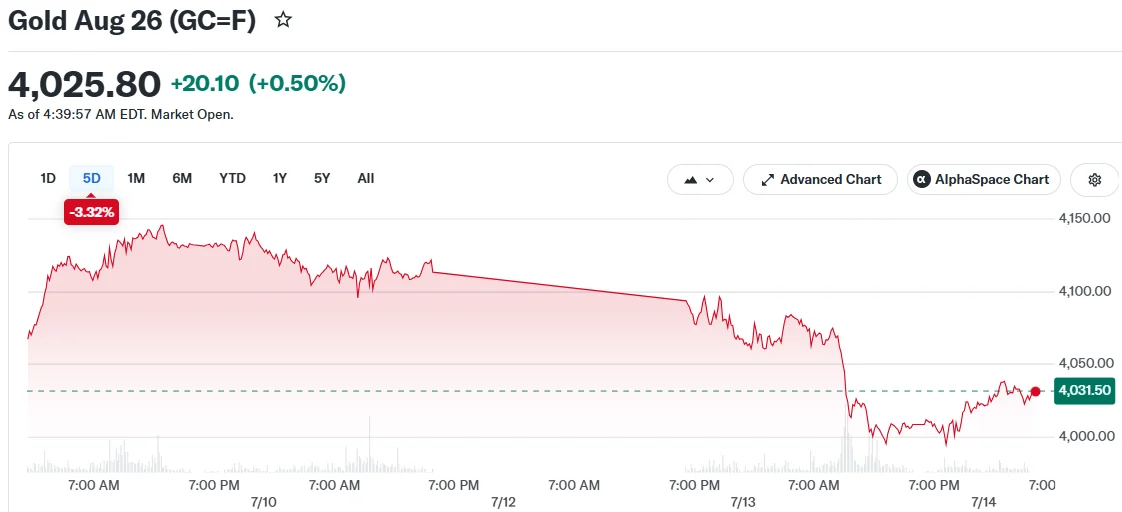

- Precious metal prices experienced significant declines Monday, with gold temporarily slipping beneath the $4,000 threshold—a level unseen in three weeks

- Silver witnessed a 3.4% decline, settling at its weakest position since early December

- Federal Reserve Governor Christopher Waller hinted at potential interest rate increases should inflationary pressures persist

- Futures markets now indicate a 43% probability of monetary tightening at the late July Federal Reserve policy meeting

- A Tuesday rebound saw gold appreciate 0.54% to reach $4,022.87, as market participants anticipate crucial U.S. inflation figures and testimony from Fed Chair Kevin Warsh

Precious metals experienced volatile trading this week as market participants grappled with mounting inflation concerns, geopolitical developments in the Middle East, and the prospect of tighter U.S. monetary policy.

Comex gold futures for July settlement plummeted 2.6% Monday, finishing at $3,997 per ounce. This marked the most substantial single-session percentage loss since late June and represented the second-weakest closing price for the yellow metal in 2025.

Silver experienced an even steeper decline. July silver contracts tumbled 3.4% to settle at $57.634 per ounce, marking the lowest closing value since December 4. Year-to-date performance shows silver trailing with a 17.8% decline, compared to gold’s 7.6% loss.

Geopolitical Developments Compound Selling Pressure

The precious metals selloff coincided with heightened geopolitical tensions in the strategically vital Persian Gulf region. President Donald Trump announced the restoration of a naval blockade targeting Iranian maritime commerce and proclaimed American forces as protectors of the Strait of Hormuz. His administration proposed imposing a 20% transit fee on cargo vessels navigating the critical waterway.

This policy shift cast uncertainty over the June ceasefire agreement and propelled petroleum prices upward. Elevated energy costs sparked renewed anxiety about persistent inflationary conditions.

Crude prices continued climbing as market participants evaluated potential supply chain disruptions through the Strait of Hormuz. This development amplified concerns that energy-linked inflation might delay Federal Reserve rate reduction plans.

For gold investors, rising energy costs present conflicting dynamics. While they can enhance gold’s attractiveness as an inflation hedge, simultaneous increases in dollar strength and Treasury yields typically pressure precious metal valuations.

Market Anticipates Potential Fed Policy Shift

Federal Reserve Governor Christopher Waller indicated that central bank officials might need to implement rate increases in the near term should inflation demonstrate persistent broad-based momentum. His remarks elevated market expectations for tightening monetary policy.

According to ANZ analysts, derivative markets now reflect a 43% likelihood of an interest rate hike during the Federal Reserve’s July 28-29 policy deliberations. Elevated borrowing costs diminish the appeal of non-interest-bearing assets such as gold.

Gold staged a modest recovery Tuesday, advancing 0.54% to $4,022.87 per ounce. Silver similarly rebounded, climbing 0.63% to $58.02. Market attention focused on forthcoming June U.S. consumer price index figures and congressional testimony from Fed Chair Kevin Warsh for monetary policy direction.

Michael Cuggino from the Permanent Portfolio Family of Funds emphasized that gold’s fundamental long-term outlook remains robust, citing sustained central bank accumulation from nations including Poland, China, and Russia. He observed that the recent selloff intensified following Warsh’s appointment, as market participants anticipated potentially higher interest rates.

Cuggino further noted that silver’s more pronounced decline reflects its extensive industrial applications across technology sectors, semiconductor manufacturing, and residential construction, rendering it particularly vulnerable to economic growth anxieties.

Investors remain focused on Warsh’s upcoming congressional testimony and inflation data releases for definitive signals regarding the Federal Reserve’s forthcoming policy trajectory.

Get 3 Free Stock Ebooks

Discover top-performing stocks in AI, Crypto, and Technology with expert analysis.

- Top 10 AI Stocks - Leading AI companies

- Top 10 Crypto Stocks - Blockchain leaders

- Top 10 Tech Stocks - Tech giants