Key Takeaways

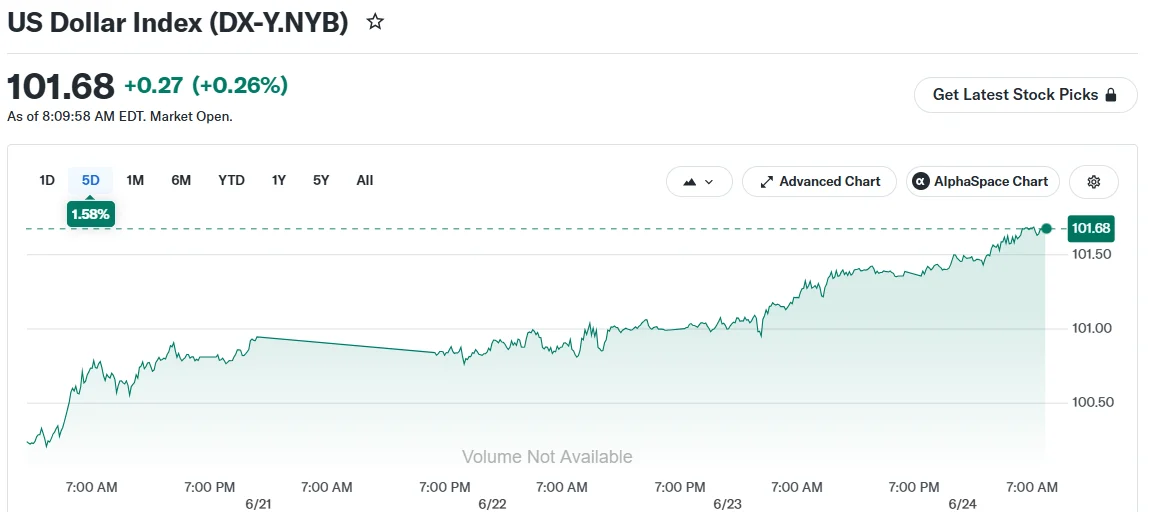

- The greenback surged to 101.63, marking its strongest performance since May 2025, with year-to-date gains approaching 3.3%.

- Investor flight to safety intensified following a technology sector collapse that eliminated over $1.3 trillion in market capitalization.

- Market participants anticipate at least two additional Federal Reserve interest rate increases in 2026, with September showing 60% probability.

- The European common currency touched 12-month lows while Japan’s yen hovers near four-decade weakness levels.

- Currency strength threatens profitability for major U.S. corporations, particularly tech giants generating half their revenues internationally.

A massive technology sector downturn that eliminated more than $1.3 trillion across two trading days triggered substantial flight-to-safety flows into the U.S. dollar on Wednesday, propelling the currency to its strongest level in over twelve months.

The benchmark Dollar Index touched 101.63 during Wednesday’s trading, representing a 0.2% intraday advance. Year-to-date performance now stands at approximately 3.3%. Tuesday’s peak of 101.69 marked the currency’s most robust reading since May 2025.

The greenback’s ascent persisted even as domestic equities mounted an early Wednesday recovery. This durability suggests the currency rally extends beyond merely reacting to technology sector weakness.

Central Bank Policy Bolsters Greenback Appeal

Market pricing indicates expectations for no fewer than two additional Federal Reserve monetary tightening moves before year-end. Derivative contracts reflect 60% probability for a September rate adjustment and nearly 40% likelihood of action as soon as July.

New Federal Reserve Chairman Kevin Warsh has consistently communicated a restrictive policy bias. This messaging has elevated speculative dollar positioning to levels last observed in early 2025, according to LPL Financial data.

Technical strategists note that a decisive breach above the 100.64 threshold could propel the index toward 105. Downside support exists near the 20-day moving average around 99.75.

Persistent price pressures combined with robust consumer spending maintain an open pathway for additional rate increases, enhancing the dollar’s attractiveness for yield-seeking international capital.

International Currencies Under Strain

The European common currency declined for its third consecutive session, reaching its weakest position versus the dollar in more than twelve months. The European Central Bank faces competing pressures from residual inflation stemming from a recent three-month conflict and emerging economic deceleration signals.

Japan’s currency remained anchored near four-decade nadirs. The dollar-yen exchange rate climbed 0.1% to 161.70. Japanese authorities have deployed approximately $72 billion in foreign exchange intervention efforts. This week featured discussions between Japan’s finance minister and U.S. Treasury Secretary Scott Bessent.

The Bank of Japan implemented a rate increase to 1.0% last week, representing the highest benchmark since the mid-1990s, yet currency recovery remains elusive.

China’s renminbi also weakened after the People’s Bank of China established a softer daily reference rate for the fourth consecutive session. Australia’s dollar held steady despite inflation readings exceeding forecasts.

Implications for Domestic Equity Markets

Currency appreciation presents challenges for corporations with substantial international operations. Roughly one-third of S&P 500 aggregate revenues originate from foreign markets.

For the Magnificent Seven technology behemoths, that proportion escalates to approximately 50%. Nvidia derives 53% of revenue from international sources. Meta generates nearly two-thirds of sales beyond U.S. borders.

When international earnings undergo conversion to dollars, greenback strength diminishes their reported value. This dynamic could pressure earnings projections, which currently anticipate second-quarter expansion of 23% and full-year growth exceeding 25%.

Get 3 Free Stock Ebooks

Discover top-performing stocks in AI, Crypto, and Technology with expert analysis.

- Top 10 AI Stocks - Leading AI companies

- Top 10 Crypto Stocks - Blockchain leaders

- Top 10 Tech Stocks - Tech giants