Key Takeaways

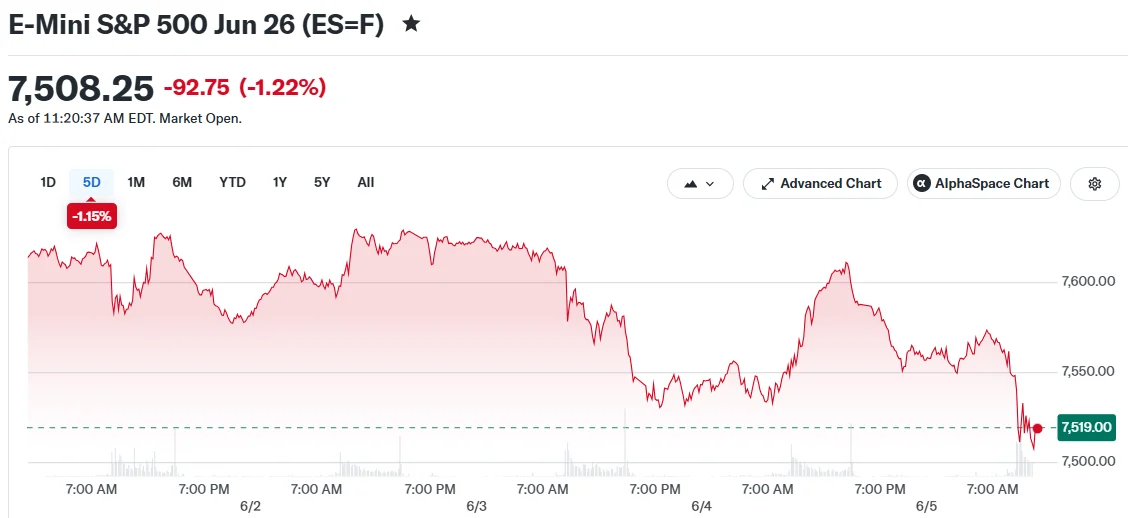

- Major indexes declined Friday with Nasdaq losing 2.1%, S&P 500 down 1.1%, and Dow shedding 140 points

- Employment report revealed 172,000 new positions in May, significantly exceeding the 88,000 consensus estimate

- Robust employment figures elevated rate increase probability to 68.3%, eliminating prospects for imminent cuts

- Semiconductor stocks tumbled further following Broadcom’s disappointing post-earnings reaction

- The S&P 500 faces potential end to 9-week rally, which would have been the longest since the mid-1980s

Equity markets experienced significant downward pressure Friday as employment data exceeded forecasts, triggering renewed speculation about monetary policy tightening while technology shares faced mounting headwinds.

The Nasdaq Composite plummeted 2.1%. The S&P 500 declined 1.1%. The Dow Jones Industrial Average retreated approximately 140 points, representing a 0.3% decrease.

The market downturn resulted from two distinct pressures converging simultaneously.

Employment Data Surprises

The May nonfarm payrolls figures revealed American businesses created 172,000 positions during the month. Market analysts had anticipated approximately 88,000 new jobs. The jobless rate remained unchanged at 4.3%.

The unexpectedly strong employment numbers dramatically altered Federal Reserve policy expectations. Market participants rapidly adjusted positions to account for potential monetary tightening.

Probability of a rate increase surged to 68.3%, climbing from 50.4% recorded the previous trading session. This development essentially eliminates near-term possibilities for policy easing.

Eric Winograd, chief US economist at AllianceBernstein, said the data shows the economy is still holding up. “That’s enough to keep the Fed on hold,” he wrote.

This development unfolds as President Trump maintains public pressure for accommodative policy. Kevin Warsh, Trump’s appointee, has recently assumed leadership at the Federal Reserve.

Semiconductor Sector Faces Renewed Pressure

Broadcom shares had already experienced sharp declines Thursday after releasing quarterly results. Friday brought additional selling pressure.

The wider semiconductor industry mirrored these losses. Market participants have grown increasingly skeptical about artificial intelligence investment sustainability, with Broadcom’s performance amplifying these doubts.

Technology equities had experienced robust gains throughout recent trading sessions, providing substantial support to benchmark indexes. That upward trajectory has now encountered significant resistance.

The Nasdaq had emerged as a primary beneficiary of AI-related enthusiasm. It now faces the steepest corrections as market sentiment reverses.

Historic Rally Faces Termination

The S&P 500 began Friday positioned for a tenth consecutive week of advances. Such a streak would have marked the most extended winning sequence since 1985.

That remarkable run now confronts potential conclusion.

The benchmark index has retreated as multiple challenges accumulate — monetary policy anxiety, technology sector fragility, and international tensions.

News regarding stalled US-Iran ceasefire discussions contributed to cautious market sentiment. President Trump characterized negotiations as approaching “final” stages, though considerable uncertainty persists.

Futures contracts had already indicated weakness before employment statistics emerged, with Nasdaq 100 futures demonstrating the steepest early declines.

The confluence of robust labor market conditions, hawkish policy expectations, and wavering AI sector confidence left limited refuge for equity investors Friday.

Get 3 Free Stock Ebooks

Discover top-performing stocks in AI, Crypto, and Technology with expert analysis.

- Top 10 AI Stocks - Leading AI companies

- Top 10 Crypto Stocks - Blockchain leaders

- Top 10 Tech Stocks - Tech giants