Key Takeaways

- The U.S. dollar index climbed to a 13-month high of 101.8, driving the euro beneath $1.14 and sending the pound to its weakest point in seven months

- Market participants now anticipate at least one Federal Reserve rate increase by October, a dramatic reversal from previous cut expectations

- Bitcoin tumbled under $60,000 for the first time this year while gold momentarily slipped below $4,000 per ounce

- Thursday’s release of core PCE data for May is anticipated to show 3.4% inflation — significantly above the Fed’s 2% objective

- Japan remains on alert for possible currency market intervention as the yen trades near four-decade lows at approximately 161.79 against the dollar

The U.S. dollar is positioned to record its most substantial monthly advance in almost twelve months, driven by mounting expectations that the Federal Reserve will raise interest rates before 2026 concludes.

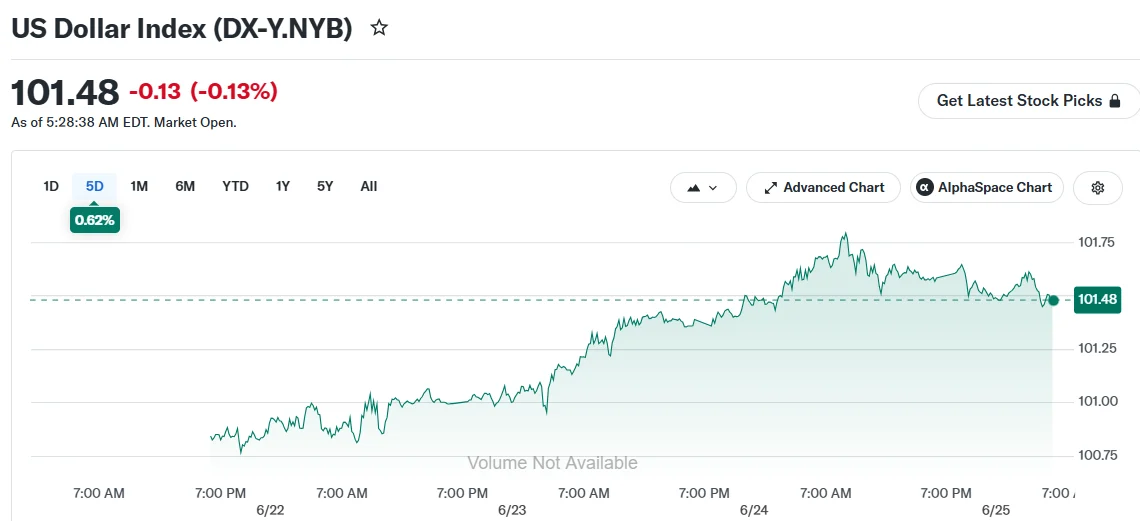

The dollar index, a measure of the greenback’s performance against six leading currencies, reached a 13-month pinnacle of 101.8 on Wednesday before moderating to roughly 101.60 on Thursday.

The euro descended below the $1.14 threshold, marking its lowest valuation in more than twelve months. The British pound declined to $1.314, reaching depths unseen since November. Both currencies experienced modest recovery on Thursday but continued facing downward pressure.

The Japanese yen remained near 161.79 versus the dollar, hovering close to its most vulnerable position in four decades. Market observers and strategists are monitoring developments for any indication that Japanese officials might intervene to bolster their currency.

“Given the accumulation of yen shorts, we would expect the impact to be significant if intervention were to be carried out,” said Hirofumi Suzuki, currency strategist at SMBC in Tokyo.

Hawkish Fed Expectations Propel Greenback

The transformation in market outlook has been dramatic. During the initial months of this year, investors broadly anticipated Federal Reserve rate reductions. Currently, markets are factoring in no fewer than one rate hike by October, with approximately 50% probability of a second increase before year’s end.

This pivot follows escalating U.S.-Israeli military tensions with Iran, which intensified inflationary concerns and diminished arguments for loosening monetary policy.

Two-year U.S. Treasury yields, which mirror near-term rate projections, have climbed nearly 14 basis points during this month to reach 4.15%. This contrasts with merely a 2 basis point increase in German yields and an almost 9 basis point decline in UK gilt yields, expanding the differential that enhances dollar-denominated asset appeal.

MUFG currency strategist Lee Hardman noted the market is unambiguously wagering the Fed will “back up tough talk on inflation by hiking rates this year.”

Digital Assets and Precious Metals Succumb to Dollar Strength

The dollar’s ascent has sent shockwaves through alternative asset classes. Bitcoin dropped beneath the $60,000 threshold for the first time since 2024, pressured by the strengthening dollar and evolving risk sentiment.

Gold temporarily fell under the $4,000 per ounce mark for the first time in over seven months before staging a modest rebound.

Critical PCE Inflation Report Awaited

Market attention has intensified around Thursday’s release of the core Personal Consumption Expenditures price index for May. Economists surveyed by Reuters project an increase to 3.4%, substantially exceeding the Federal Reserve’s 2% inflation target.

An elevated reading could amplify dollar gains further, while a softer-than-expected number might provide temporary respite for competing currencies.

The Australian dollar edged down 0.12% to approximately $0.69 following inconclusive employment data. The New Zealand dollar likewise remained near seven-month troughs, with both antipodean currencies responding primarily to U.S. interest rate expectations.

Get 3 Free Stock Ebooks

Discover top-performing stocks in AI, Crypto, and Technology with expert analysis.

- Top 10 AI Stocks - Leading AI companies

- Top 10 Crypto Stocks - Blockchain leaders

- Top 10 Tech Stocks - Tech giants