Key Takeaways

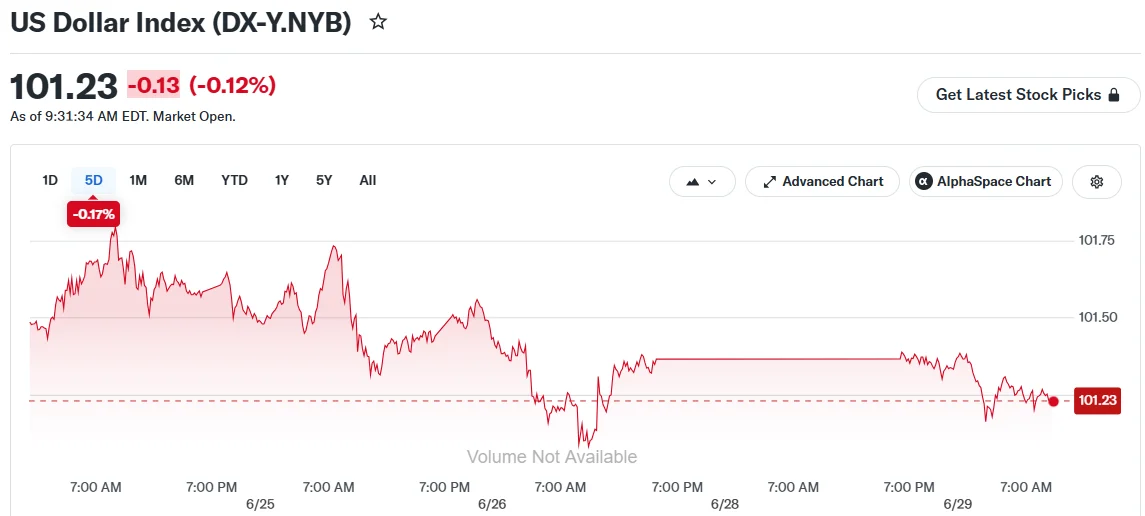

- The U.S. Dollar Index retreated to 101.24 but hovers close to a 14-month peak

- June marks the greenback’s strongest monthly performance since July 2025, climbing approximately 2.5%

- Diplomatic negotiations between Washington and Tehran in Qatar are reducing safe-haven currency flows

- Market participants anticipate two additional Federal Reserve rate increases through year-end amid inflation exceeding 4%

- This week’s spotlight falls on the ECB Sintra Forum and crucial U.S. employment figures

The greenback experienced a modest retreat Monday while maintaining its position near a 14-month peak. Trading at 101.24 during early North American sessions, the U.S. Dollar Index edged lower from its June 24 high of 101.8.

The minor correction hasn’t diminished the currency’s impressive trajectory this month. June remains on track to deliver the dollar‘s most substantial monthly advance since July 2025, with gains hovering around 2.5%.

Forces Behind the Dollar’s Ascent

Multiple catalysts have sustained the greenback’s elevated position. With U.S. inflation persisting above the 4% threshold, the Federal Reserve faces mounting pressure to maintain its hawkish monetary posture. Financial markets have priced in two additional quarter-point rate increases before December arrives.

Robust economic indicators from the United States have reinforced this narrative. A durable employment landscape has bolstered investor confidence in dollar-backed assets, with Friday’s upcoming non-farm payrolls data positioned as a critical barometer for future direction.

Investment flows targeting U.S. artificial intelligence equities have contributed meaningfully as well. International capital gravitating toward American technology markets has sustained consistent demand for dollar-denominated instruments.

International Tensions and Monetary Policy Coordination

The recent U.S.-Iran conflict served as a significant catalyst for safe-haven dollar accumulation throughout recent sessions. Following weekend hostilities, both nations agreed to suspend military operations, with diplomatic discussions scheduled to reconvene in Qatar on Tuesday.

The ceasefire agreement has begun alleviating strain across global commodity markets. Petroleum prices have retreated toward pre-escalation benchmarks as shipping activity through the Persian Gulf normalizes following a bilateral understanding between American and Iranian authorities.

The euro registered a 0.2% increase to $1.14 but continues trading near its annual low. Sterling maintained stability at $1.32 as Britain navigates significant political change. Following Keir Starmer’s resignation announcement last week, Andy Burnham has emerged as the leading candidate for succession.

The European Central Bank’s prestigious Sintra Forum commences Monday. ECB President Christine Lagarde will share the platform with Fed Chair Kevin Warsh and Bank of England Governor Andrew Bailey for opening statements. Market consensus anticipates at least one additional ECB rate adjustment this year following the recent deposit rate elevation to 2.25%.

The Japanese yen showed minimal movement. Japan’s forthcoming Bank of Japan Tankan survey is anticipated to reveal enhanced corporate sentiment despite recent energy market disruptions.

Throughout Asian markets, analysts are monitoring China’s manufacturing indicators, South Korea’s trade statistics, and India’s industrial output figures for insights into regional central bank trajectories.

The dollar’s near-term direction hinges largely on central bank communications emerging from Sintra and the employment data release concluding this week.

Get 3 Free Stock Ebooks

Discover top-performing stocks in AI, Crypto, and Technology with expert analysis.

- Top 10 AI Stocks - Leading AI companies

- Top 10 Crypto Stocks - Blockchain leaders

- Top 10 Tech Stocks - Tech giants