TLDR

- Following disappointing June employment figures, the greenback stabilized near two-week lows as Fed rate hike expectations declined

- Japan’s currency hovers near four-decade lows around 161-162 versus the dollar, maintaining intervention concerns

- This week’s Federal Reserve meeting minutes expected, though new Chair Kevin Warsh’s approach may limit forward guidance

- The European single currency maintained levels near $1.1435 while the British pound traded around $1.3351, both declining modestly Monday

- Seoul initiated groundbreaking round-the-clock onshore dollar-won spot markets on Monday

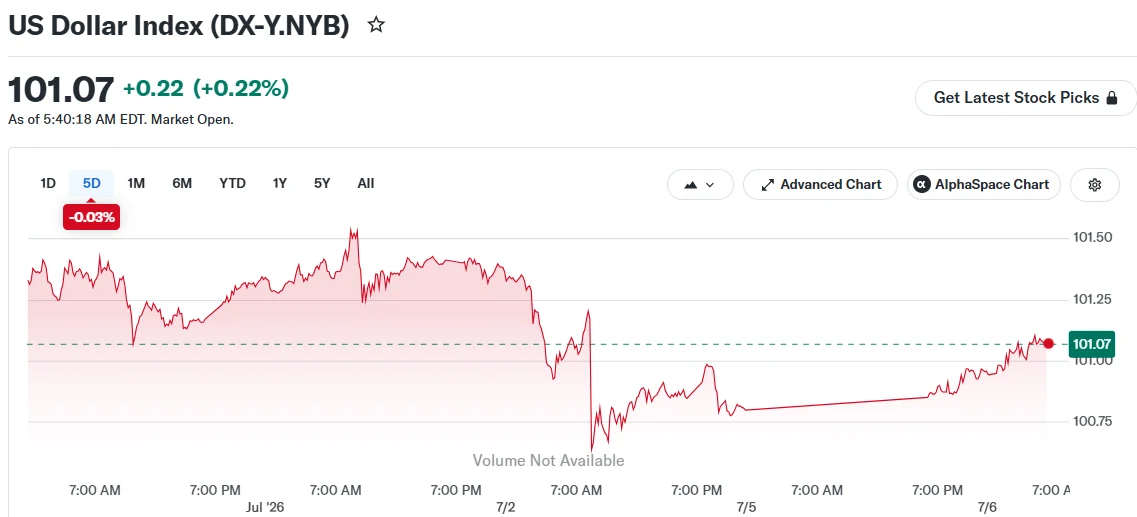

The greenback saw modest gains Monday while remaining near its lowest point in two weeks, following last week’s disappointing U.S. employment data that diminished prospects for additional Federal Reserve interest rate increases. Meanwhile, Japan’s currency lingers precariously near four-decade lows, maintaining market vigilance for potential government market intervention.

Greenback Faces Headwinds Following Employment Report

The dollar index, measuring the U.S. currency against a basket of six major counterparts, traded around 100.9 during early Monday sessions. This followed a 0.5% weekly decline — marking its steepest weekly retreat since April.

The catalyst came from June’s nonfarm payrolls data, revealing significantly slower employment expansion. This development sparked doubts about whether the Federal Reserve possesses sufficient justification to continue tightening monetary policy.

However, the dollar’s decline was limited. The jobless rate actually decreased, which OCBC strategists noted indicates continuing labor market tightness. They preserved their forecast of modest 2-3% dollar strengthening during the latter half of 2026.

The European single currency stood at $1.1435, close to two-week peaks. The British pound traded at $1.3351. Both currencies retreated approximately 0.1% Monday as the dollar recovered slightly.

Declining oil prices have contributed to reduced inflation worries, further supporting diminished rate increase expectations.

Market attention now shifts to this week’s release of the Federal Reserve’s June meeting minutes. Officials at that gathering reportedly displayed more hawkish tendencies due to persistent inflation pressures.

Nevertheless, newly appointed Fed Chair Kevin Warsh has indicated the central bank has provided excessive forward guidance historically. Commonwealth Bank of Australia analysts cautioned the minutes might deliver less clarity than typically expected.

Japanese Currency Approaches Four-Decade Nadir, Intervention Speculation Persists

Japan’s currency traded between 161.57-161.82 per dollar Monday, barely off the 162.84 threshold reached last week — representing the weakest position since 1986.

The Bank of Japan implemented rate increases in June while signaling additional hikes remain possible. Nevertheless, the substantial interest rate differential between the United States and Japan continues exerting considerable downward pressure on the yen.

Japanese authorities have issued verbal cautioning against speculative selling of their currency in recent weeks. Tokyo last conducted market intervention during late April and early May, driving the dollar-yen exchange rate down toward 155. The pair rapidly rebounded above 160.

Analysts remain split regarding whether fresh intervention efforts would produce lasting impacts. OCBC strategists suggested intervention by itself probably cannot reverse the pair’s trajectory without genuine changes in underlying economic conditions.

ING analysts emphasized that more hawkish messaging from the Bank of Japan remains necessary to prevent dollar-yen from advancing further.

Marc Chandler of Bannockburn Global Forex observed that options market behavior suggests major investors have purchased short-dated dollar puts as insurance against unexpected intervention actions.

In other developments, South Korea’s won remained stable as Seoul introduced round-the-clock onshore dollar-won trading, representing progress toward achieving developed market designation on the MSCI index. China’s yuan and Singapore’s dollar both weakened marginally.

Get 3 Free Stock Ebooks

Discover top-performing stocks in AI, Crypto, and Technology with expert analysis.

- Top 10 AI Stocks - Leading AI companies

- Top 10 Crypto Stocks - Blockchain leaders

- Top 10 Tech Stocks - Tech giants